UK Defence: Nuclear, Naval and Digital primes in focus

We expect UK MoD incumbents such as BAE Systems, Rolls-Royce and Babcock outperform driven by exposures to the nuclear, naval and digital/space capabilities

Summary

While we await the Defence Investment Plan (DIP), we lay out a framework to analyse where the UK defence budget is most likely to translate into investable opportunities. With roughly 45% of the £60.2bn defence budget tied to equipment expenditure, the key question is how this spending is allocated across various capability gaps. Among the major UK and international prime contractors, we believe the most compelling opportunities lie where these capability gaps intersect with MoD incumbency and long-cycle programme exposure.

We see the strongest read-through in Nuclear, Naval and Digital segments. Nuclear should remain the most protected segment, given its role in sovereign deterrence, Dreadnought renewal, SSN-AUKUS, and nuclear propulsion. Naval should benefit from submarine commitments, maritime surveillance and undersea infrastructure protection. Digital should gain importance as cyber, electromagnetic warfare, secure communications, space resilience and battlefield networks become core combat-enabling capabilities. We remain most positive on BAE Systems, Rolls-Royce and Babcock, given their exposure to these segments and their market-leading position in securing largely non-competitive contracts with the MoD.

This article is the third of a three‑part series on UK Defence. For a more detailed deep dive on the Strategic Defence Review (SDR) and execution challenges faced by the UK MoD, refer to our earlier notes.

Table of Contents

Incumbency is key

1.1 High barriers to entry

1.2 Spending concentration

Prime contractors

2.1 UK-listed contractors

2.2 Private and international contractors

What’s in the budget

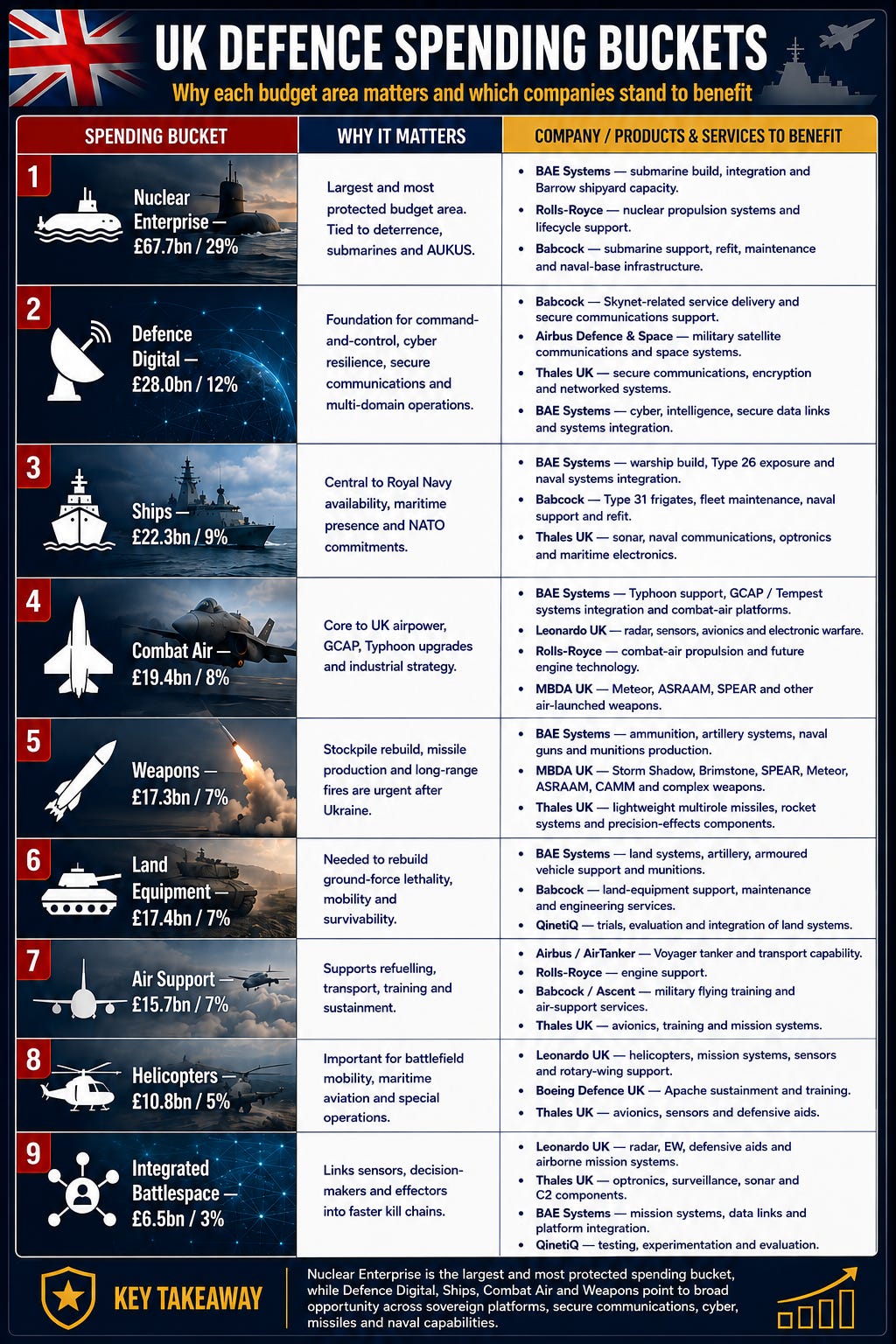

3.1 Budget breakdown

3.2 Equipment expenditure guidance

Capability mapping

4.1 Contractors per spending bucket

4.2 Nuclear, Naval, Combat Air and Digital

Investment implications

5.1 Assessment framework

5.2 Contractor tiering

Incumbency is key

High barriers to entry: The UK defence industry is not a normal procurement market. It is structurally difficult for new entrants to displace incumbents because contracts are tied to national security, classified programmes, industrial capacity and specialist engineering depth. Contractors require high security clearances, export-control compliance, long qualification histories and trusted relationships with the MoD. This creates a powerful moat. Once a company is embedded in national defence production lines for key capabilities such as submarines, nuclear propulsion combat air and secure communications, switching contractors is difficult due to the introduction of delivery, security and operational risk. In terms of its implications, this means that the UK defence budget is unlikely to flow evenly across the sector. It should disproportionately benefit companies already inside the MoD ecosystem.

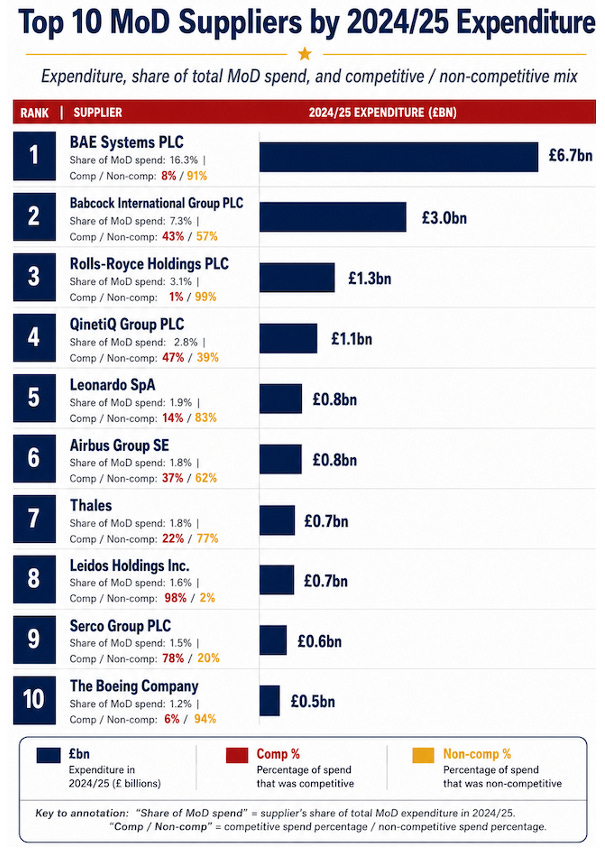

Spending concentration: In 2024/25, the ten largest private-sector holding companies that contracted more than £100m from the MoD accounted for 39.4% of total MoD expenditure. BAE Systems alone received £6.7bn (16.3%) followed by Babcock at £3.0bn (7.3%). The remaining major contractors: Rolls-Royce, QinetiQ, Leonardo, Airbus, Thales, Leidos, Serco and Boeing - each received roughly £0.5bn to £1.3bn, equivalent to 1.2% to 3.1% of total MoD expenditure.

Existing MoD contracting structures reinforce the moat. 7 out of 10 of the largest prime defence contractors capture more than 50% of MoD expenditure revenues through non-competitive routes. This reflects limited alternatives, high switching costs and sovereign capability constraints. Rolls-Royce, Boeing, BAE Systems, Leonardo, Thales and Airbus all had majority non-competitive exposure in 2024/25. In our view, this means that if UK defence spending rises, the first-order beneficiaries are likely to be incumbent contractors with embedded programmes, existing clearances and proven delivery infrastructure.

Prime contractors

The UK MoD contractor base is anchored by a small group of listed UK primes, private defence specialists and international contractors. These companies form the main contracting force behind the UK’s nuclear, naval, combat air, missile, digital, testing and support programmes. For investors, the key is to identify which contractors already sit inside long-cycle MoD programmes, because those incumbents have the clearest route from budget allocation to funded orders.

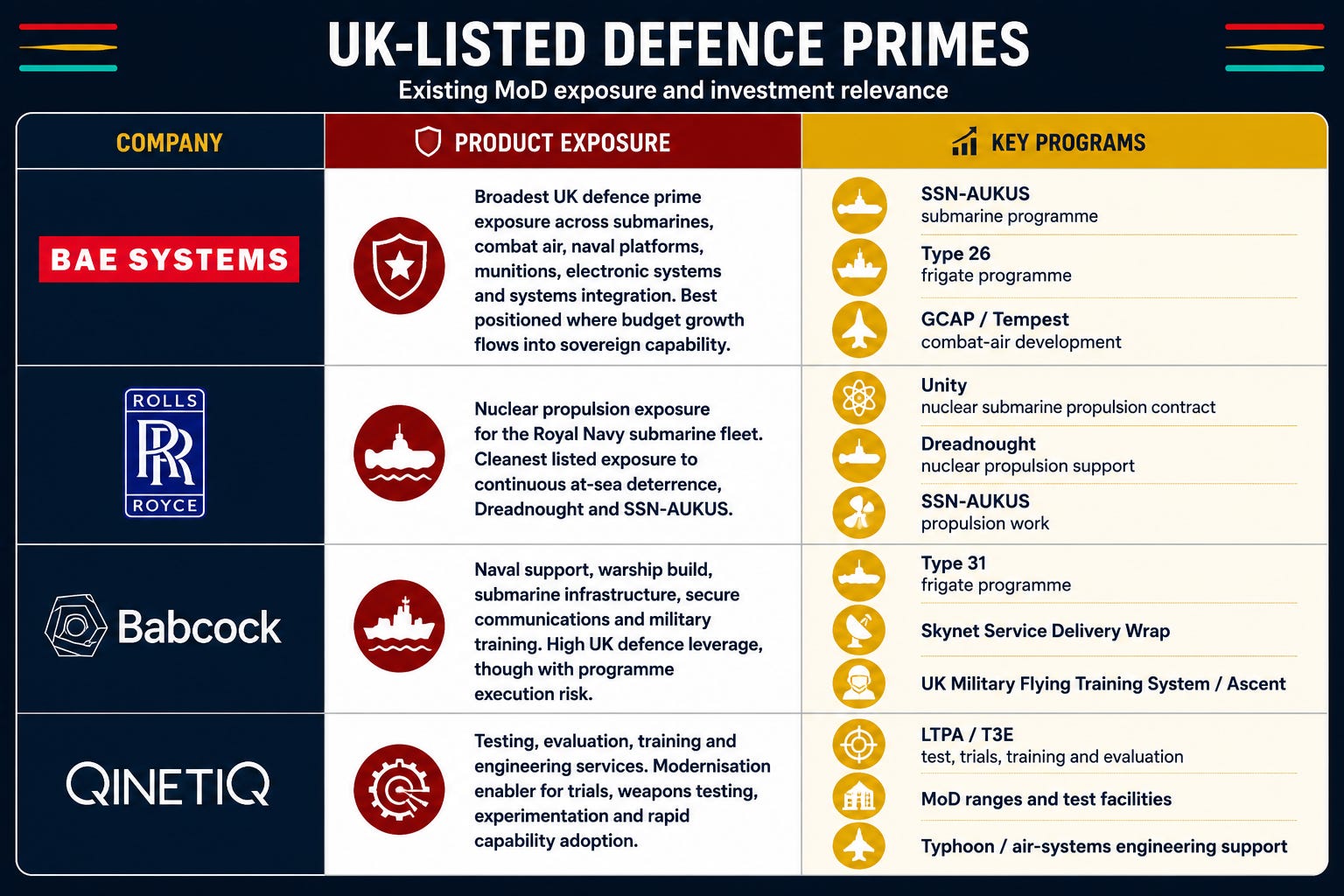

UK-listed contractors provide the cleanest public-market exposure to the defence budget. BAE Systems, Rolls-Royce, Babcock and QinetiQ are each embedded in different parts of the MoD ecosystem, but the common thread is incumbency. These companies already sit inside sovereign or long-cycle programmes where the MoD has limited ability to switch contractors quickly.

Private and international contractors provide more targeted exposure to capability-specific areas such as missiles, sensors, electronic warfare, satellite communications, air support and platform sustainment. While the captured revenue pools may be less direct than for UK-listed primes, these contractors remain strategically important to the MoD’s future capability mix.

What’s in the budget

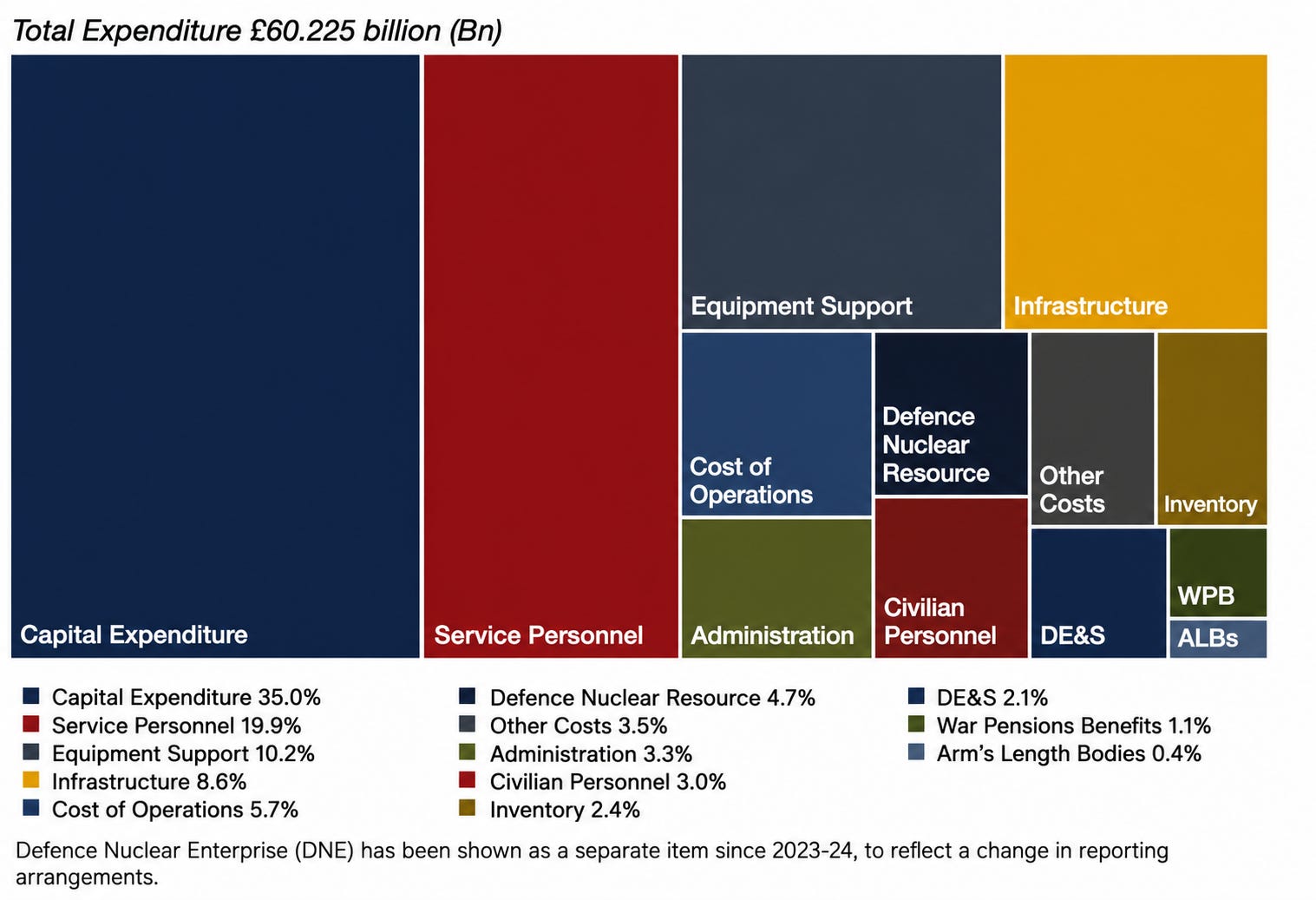

Budget breakdown: The UK defence budget totalled £60.2bn in 2025, equivalent to around 2.5% of GDP. Six categories accounted for 85% of total spending: capital expenditure, service personnel, equipment support, infrastructure, cost of operations and administration. The key area of spending we are focused on is equipment-related because it has the clearest read-through to defence company revenues. This is captured through capital expenditure (35%) and equipment support (10%). Together, these two buckets represent roughly 45% of the defence budget, or about £27bn per year. This is the core revenue pool for platforms, upgrades, sustainment, munitions, digital systems and support services.

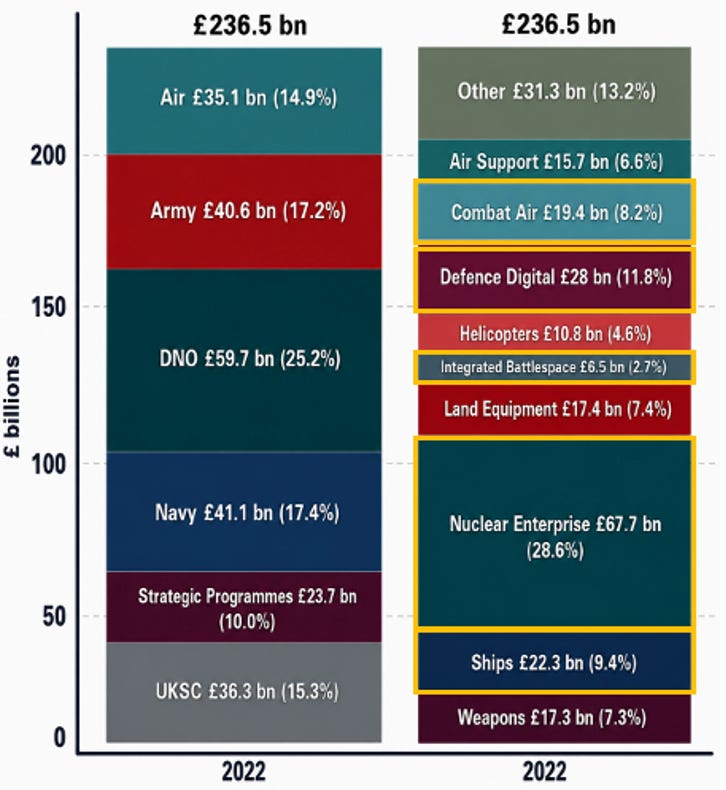

Equipment expenditure guidance: The latest full Defence Equipment Plan published by the MoD was the 2022–2032 plan. Despite the lack of a more recent update, we view the 2022 plan as useful guidance for understanding the MoD’s equipment spending priorities. While the next DIP should replace the old Equipment Plan framework, we do not expect the broad direction of spending to change materially. The key point is that the UK equipment budget remains anchored around a familiar set of capability areas: Nuclear Enterprise, Ships, Combat Air, Weapons, Defence Digital, Air Support, Land Equipment, Helicopters and Integrated Battlespace.

What we think should change is the mix. We expect Nuclear Enterprise, Ships, Combat Air and Defence Digital / Integrated Battlespace to grow as a share of total equipment spending. These areas align most closely with the UK’s priorities outlined in the Strategic Defence Review (SDR): deterrence, AUKUS, secure communications, CyberEM, AI-enabled warfare, battlefield connectivity and Global Combat Air Programme (GCAP).

Capability mapping

Contractors per spending bucket: Our investment framework starts by mapping the equipment budget to the capability gaps that matter most. The strongest opportunities should emerge where sizeable funding pools, urgent operational requirements and entrenched contractor positions intersect. On that basis, we see the Nuclear Enterprise, Digital Defence, Ships, Combat Air and Integrated Battlespace as the key spending buckets to track.

Nuclear should remain the most protected area of UK defence spending because it sits at the centre of the sovereign deterrence posture. The SDR reaffirms the UK’s commitment to a minimum, credible and independent nuclear deterrent assigned to NATO, with continuous at-sea deterrence maintained through ballistic missile submarines. The Defence Nuclear Enterprise is also undergoing a major renewal phase, including four Dreadnought-class submarines to replace the current Vanguard-class submarines, SSN-AUKUS design, nuclear infrastructure upgrades and the re-establishment of a defence nuclear fuel cycle. This creates the clearest read-through to incumbents: BAE Systems in submarine build and integration, Rolls-Royce in nuclear propulsion and reactor-related support, and Babcock in submarine support, refit, maintenance and naval base infrastructure.

Naval spending should also remain a core focus because the Royal Navy is expected to play a larger role in securing the UK’s critical undersea infrastructure and maritime trade. The SDR calls for enhanced maritime surveillance, closer cooperation with government and commercial partners, and a more modern maritime force built around hybrid carrier air wings, autonomous collaborative platforms, single-use drones and long-range missiles. Anti-submarine warfare is also a priority, with greater integration of underwater, surface and airborne drones alongside Type 26 frigates, P-8 maritime patrol aircraft and SSN attack submarines. This supports demand across submarines, surface ships, maritime surveillance and autonomous systems. Our read-through is to BAE Systems in Type 26 and submarines, Babcock in Type 31 and refit, and Thales UK in sonar and naval electronics.

A key adjacency to naval capabilities is the Combat Air segment. What fall’s in scope here is aerial missile defence (launched from naval vessels) and aircraft carrier capabilities. Given the UK’s geography, key air-defence threats are likely to come from long-range missiles, drones, hostile aircraft and naval-launched systems across the Euro-Atlantic and maritime theatres. The SDR highlights the need for closer integration between the Royal Navy, carrier air wings, autonomous platforms, long-range missiles and integrated air and missile defence. GCAP reinforces this direction, with the UK, Italy and Japan developing a sixth-generation air system built around uncrewed platforms, next-generation weapons, networks and data sharing. We think the main beneficiaries are BAE Systems in GCAP and systems integration, Leonardo UK in radar and electronic warfare, Rolls-Royce in propulsion, and MBDA UK in air-launched weapons (SPEAR and ASRAAM) and missile defence.

Digital Defence is likely to grow in importance because it is becoming a combat-enabling capability. The SDR frames the Cyber and Electromagnetic (CyberEM) domain as central to covering offensive and defensive cyber activity, electronic warfare, signals intelligence, jamming, communications denial and force-protection countermeasures. Space resilience is also a priority, with expected investment in military space systems that support space control, decision advantage and the ability to “understand” and “strike”, alongside reviews of SKYNET 6A and SKYNET 6C resilience. Our read-through favours contractors exposed to secure/satellite communications, cyber resilience, electronic warfare, data links, ISR and systems integration. This points to Babcock, Airbus Defence & Space, Thales UK, BAE Systems and Leonardo UK.

Investment implications

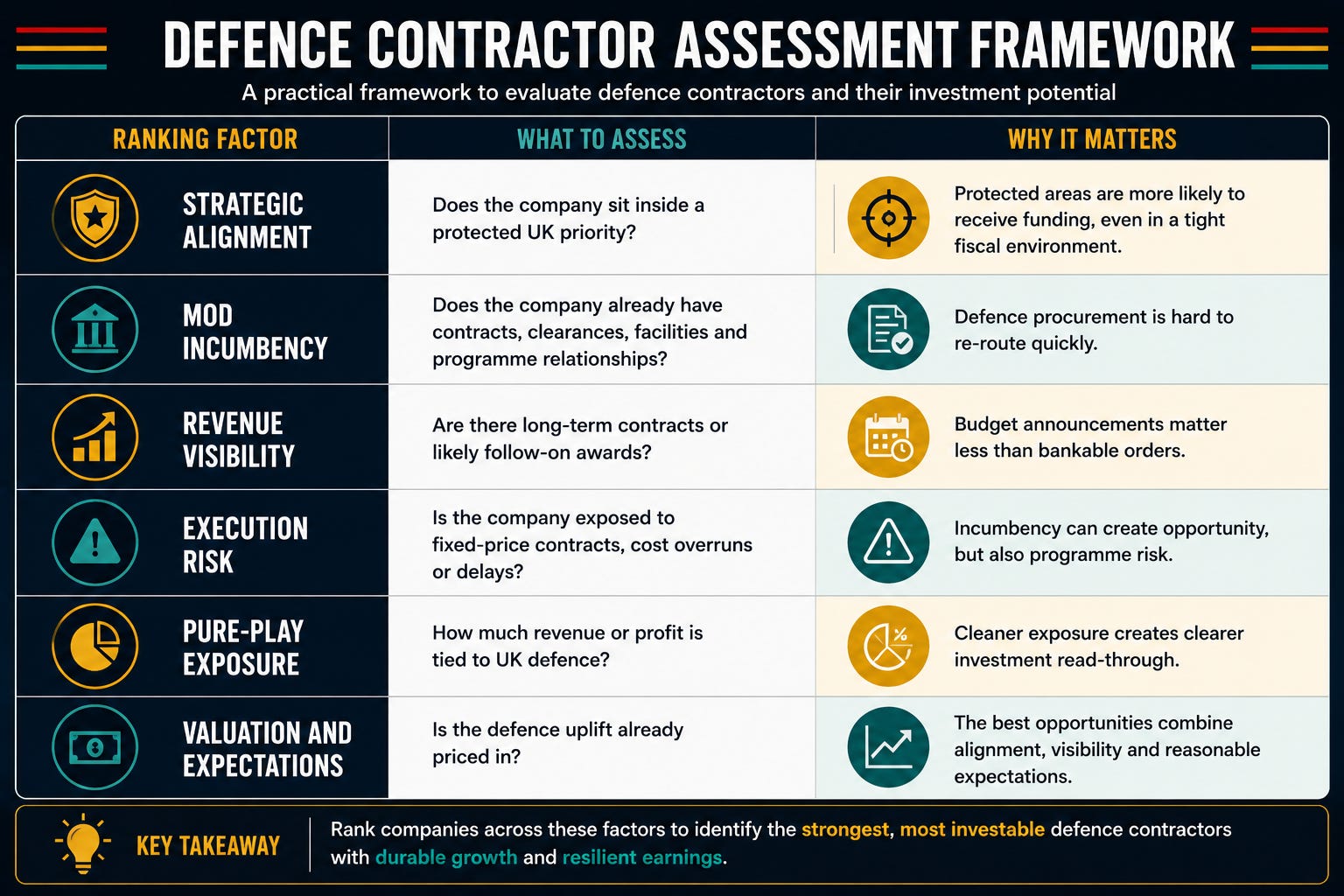

We would rank defence prime contractors across six factors: strategic alignment, MoD incumbency, revenue visibility, execution risk, pure-play exposure and valuation expectations. The strongest candidates should sit close to protected priorities. These include nuclear deterrence, submarines, combat air and digital warfare. They should also have a credible path from budget allocation to revenue. In our view, we are most positive on Tier 1 names, which have the clearest exposure to protected capability areas and long-cycle funded programmes. Lower tiers either offer more specialised exposure or higher-growth upside, but with less direct budget read-through or greater procurement risk.

The key conclusion is that the UK defence ramp-up will favour incumbents before challengers. The most relevant spending pool is not the headline defence budget, but the equipment envelope that converts into platforms, upgrades, support, munitions and digital systems. The strongest opportunities sit where this equipment spending overlaps with urgent capability gaps and entrenched MoD contractor positions. In our view, this points to Nuclear, Naval, Combat Air, and Digital Defence/ Integrated Battlespace as the most important areas to track.

Our framework leaves us most positive on BAE Systems, Rolls-Royce and Babcock. BAE offers the broadest exposure across submarines, naval platforms, combat air, munitions and systems integration. Rolls-Royce is the cleanest listed exposure to nuclear propulsion and the submarine renewal cycle. Babcock benefits from naval support, refit, submarine infrastructure and secure communications. Tier 2 contractors include QinetiQ, Leonardo UK, Thales UK and MBDA UK, where the read-through is strongest across testing, sensors, electronic warfare, missiles, air defence and battlefield digitisation. The key risk is not demand, but conversion: investors should focus on which Defence Investment Plan priorities become funded orders, and which contractors have the incumbency and execution track record to capture them.

Author’s note: This material and/or its contents are current at the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the written consent of the Author. Any view expressed herein is from the Author, is based on available information, and are subject to change without notice. While any third-party data used is considered reliable, its accuracy is not guaranteed. Forward-looking statements should not be considered as guarantees or predictions of future events. Past results are not a reliable indicator of future results. The Author assumes no duty to update any information in this material if any such information changes.