BAE Systems: The Transatlantic Prime for the Defence Supercycle

Defence incumbent with scaled exposure to the US, UK, Europe, Saudi Arabia and Türkiye, positioned across the highest-priority allied capability gaps

Summary:

BAE Systems is one of the clearest listed beneficiaries of the NATO defence upcycle. The company is positioned where global defence budgets are most likely to convert into funded, long-duration programmes. These include mission-essential capabilities such as nuclear submarines, naval shipbuilding, combat air, munitions, electronic warfare, space, cyber and secure mission systems. Its product suite serves the fundamental defence needs of the US, UK, Europe, Saudi Arabia and Türkiye as governments rebuild deterrence, replenish inventories and modernise for digitally enabled warfare.

We expect BAE’s earnings mix to improve as growth shifts toward the units most exposed to core allied capability gaps. In our view, its Electronic Systems unit, the “picks and shovels” of modern defence equipment spending, should be the largest driver of margin improvement at the group level. Its Platforms & Services unit will serve as a core growth driver, supported by direct Ukraine war demand, Sweden’s defence spending ramp-up, and US inventory restocking post Iran war across munitions and combat mission systems. We expect its Air unit to benefit from rising demand for air defence, missile systems and combat-air modernisation, supported by Middle East threat dynamics and the potential export of Golden Dome-style architectures to allied markets. Its Maritime and Cyber & Intelligence units add longer cycle visibility through submarines, naval systems, secure networks and intelligence infrastructure.

This article is the first of a two‑part series on BAE Systems. In the follow‑up note, we will focus on the company’s financial profile, forward outlook, and investment case.

Table of Contents

Global defence budget

1.1 US budget

1.2 Europe and UK budget

1.3 Saudi Arabia budget

Enter BAE Systems

Understanding the Business

3.1 Electronic Systems

3.2 Platform & Services

3.3 Air

3.4 Maritime

3.5 Cyber & Intelligence

Strategic priorities

4.1 Forward guidance

4.2 Divisional priorities

4.3 Order backlog and pipeline

Governance considerations

5.1 Management team

5.2 Board oversight

5.3 Shareholding and ownership

5.4 Capital allocation

5.5 Stakeholder management

1. Global Defence Budget

We believe global defence spending is at the beginning of a structural upcycle, underpinned by rising geopolitical risk and a shift toward higher defence readiness. We see this being driven by a more contested security environment, higher NATO burden-sharing requirements, depleted inventories and the shift toward space, cyber and digitally enabled warfare.

1.1 US Budget

The US remains the largest and most important defence market globally. The FY27 budget proposal points to a material expansion in the addressable opportunity for defence primes and suppliers, with roughly $1.5tn in national defence spending, including around $350bn of reconciliation funding. The most relevant area for the defence industrial base is Modernisation, defined as Procurement plus RDT&E, which totals around $758bn, or roughly half of the total request.

The largest areas of incremental spend are missiles and munitions, space and missile defence, shipbuilding and F-35 procurement. The request includes around $71bn for missiles and munitions procurement, around $71bn for Space Force, roughly $65.8bn for shipbuilding and a step-up in F-35 procurement to around 85 aircraft. While some of this growth depends on reconciliation funding, the direction is clear: the US budget is shifting toward modernisation, munitions, space, missile defence, maritime capacity and advanced airpower.

2.2 Europe and UK Budget

European defence spending is also entering a structurally transformative period. The Hague Summit Declaration reset NATO’s spending framework from the old 2% target toward a broader 5% defence-related commitment, split between 3.5% for core defence and 1.5% for defence-related infrastructure, resilience, civil preparedness, telecommunications and innovation. After decades of underinvestment, Russia’s war footing, uncertainty around US security guarantees and growing public support for rearmament have made higher European defence spending the new base case.

We believe the uplift will be meaningful, but uneven. Eastern Europe is likely to move the fastest, given frontline security needs. Germany will be critical given its scale and fiscal reset, while France, Italy, Spain and the Nordics will determine the breadth of the broader European procurement cycle. The UK remains one of Europe’s most important defence markets given its role as a nuclear power, NATO framework nation and advanced industrial base. The UK opportunity should be concentrated in Nuclear, Digital Defence, Ships, Combat Air and Integrated Battlespace arenas. The key risk is conversion and funding: translating higher spending ambitions into funded procurement plans and long-term industrial demand signals.

1.3 KSA Budget

The Kingdom of Saudi Arabia (KSA) remains one of the fastest growing defence markets globally and the leading military power in the Middle East. The Kingdom has allocated roughly $78bn for defence spending in 2025, up from $75bn in 2024, with defence representing more than 20% of total government spending. The addressable market is supported by Saudi Arabia’s need to sustain airpower, modernise land and naval capabilities, strengthen missile and air defence, and invest in infrastructure, training, maintenance and support.

In our view, the key structural driver is the Vision 2030 plan. Saudi Arabia aims to localise 50% of defence procurement by 2030, versus its domestic defence share of 19% today. This shifts the market from pure imports toward joint ventures, local manufacturing, technology transfer and industrial partnerships. While the opportunity remains large, the path towards monetisation will be complex. Among regulatory hurdles, we think contractors will need to navigate localisation requirements, licensing, export controls, local partnerships and case-by-case procurement negotiations.

2. Enter BAE Systems

BAE Systems is the UK’s largest defence contractor and one of the most strategically important defence primes in the Western alliance. Today, BAE’s revenue base is concentrated in the largest defence markets globally, with its sales led by the US (43%) and UK (27%), Europe (12%), the Kingdom of Saudi Arabia (9%), Australia (4%) and other international markets (5%).

The company was formed on 30 November 1999, when British Aerospace and Marconi Electronic Systems merged to create a UK defence champion that combined platform expertise with defence electronics, radar, sensors and electronic warfare capabilities. The merger was a direct response to post-Cold War defence consolidation, particularly in the US, where companies such as Lockheed Martin and Boeing had scaled into global defence giants. In our view, BAE was created to ensure the UK retained a prime contractor with the scale, systems expertise and sovereign capability needed to compete globally.

The strategic logic of the merger still defines BAE today. British Aerospace brought aircraft, shipbuilding and defence manufacturing capabilities. Marconi Electronic Systems added higher-value electronics, sensors, radar, communications and electronic warfare. The result was not simply a larger defence company, but a systems contractor capable of designing, building, upgrading and supporting complex military platforms. This model has become increasingly relevant as warfare shifts from standalone platforms toward connected, software-enabled and electronically protected combat systems.

Post 2010, BAE expanded aggressively into the US to build access in the world’s largest defence market. The company pursued a “home market” strategy, supported by acquisitions such as United Defence in 2005 and Armor Holdings in 2007. This transformed BAE from a UK-centred contractor into a transatlantic prime with meaningful exposure to both the UK MoD and US Department of Defence. Over time, BAE has shifted from being primarily a platform manufacturer toward a broader defence systems, sustainment and mission-technology company. It remains embedded in long-cycle programmes such as F-35, Typhoon, Dreadnought submarines, Type 26 frigates and Future Combat Air Systems (FCAS). It has also expanded into electronic warfare, cyber, space, sensors, secure communications and digital engineering, reinforced by the 2024 acquisition of Ball Aerospace.

BAE’s strategic identity is therefore best understood through three lenses. First, it is the UK’s core sovereign defence prime, with irreplaceable roles in submarines, naval platforms, combat air and munitions. Second, it is a transatlantic defence contractor with significant exposure to the US, Europe and the Middle East. Third, it is increasingly a mission-systems company, where electronics, cyber, space, data and software are becoming as important as the platforms themselves. This makes BAE one of the cleanest public-market exposures to the UK and allied defence investment cycle.

BAE’s history explains its moat: The company was built to preserve national industrial capability, and that role has only become more important as the allied forces rebuild their defence capacity for a more contested security environment.

3. Understanding the Business

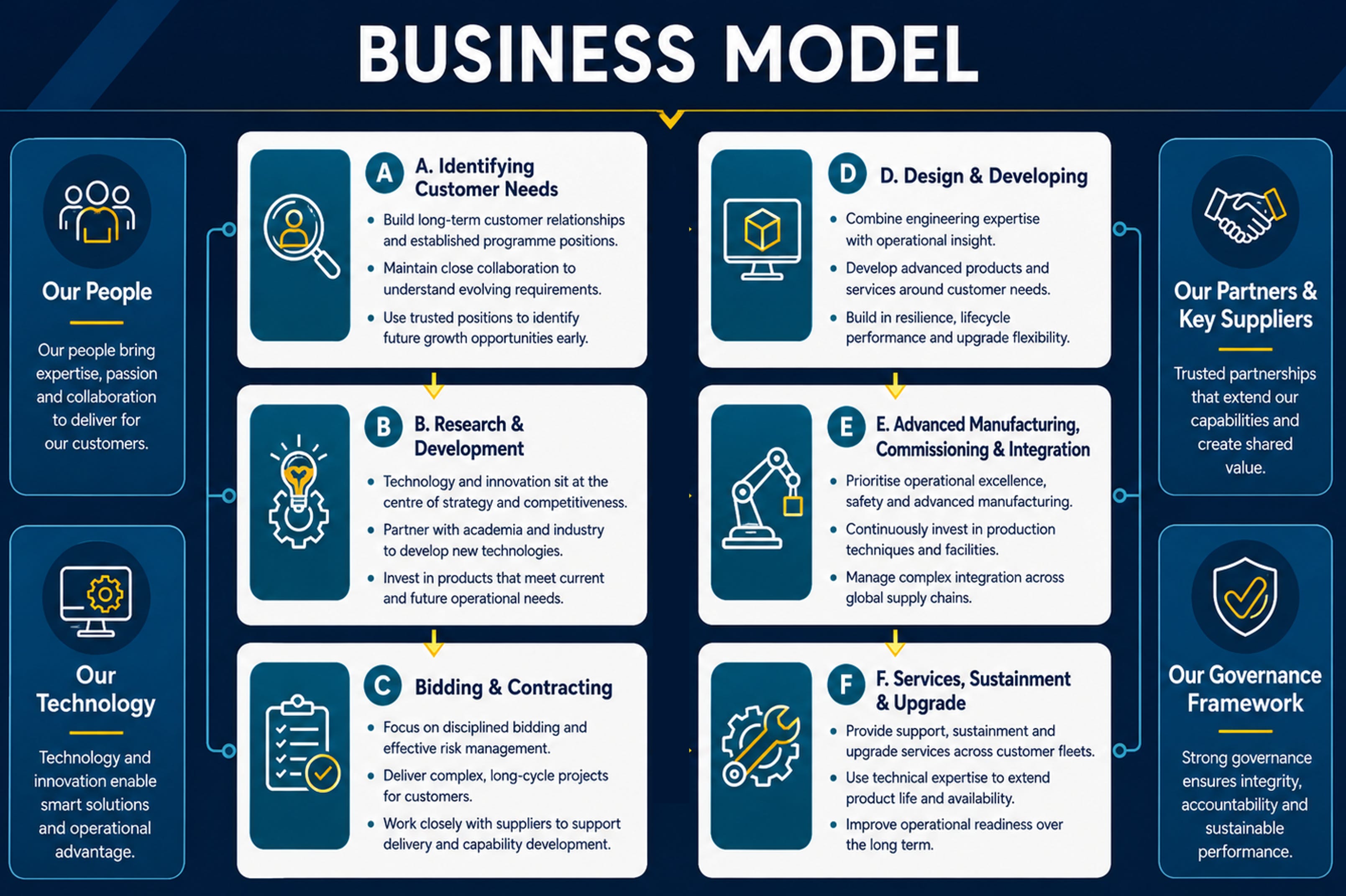

BAE’s business model is built around long-cycle defence programmes where customer relationships, technical depth and delivery credibility compound over time. The company identifies capability gaps, invests in proprietary technology, and generates revenue across design, development, manufacturing, integration, sustainment and upgrades. This creates a lifecycle revenue model rather than a one-off equipment sale. In our view, this is central to BAE’s moat: once embedded in a customer’s defence architecture, the company becomes difficult to displace given switching costs, classified know-how and the need for long-term operational support.

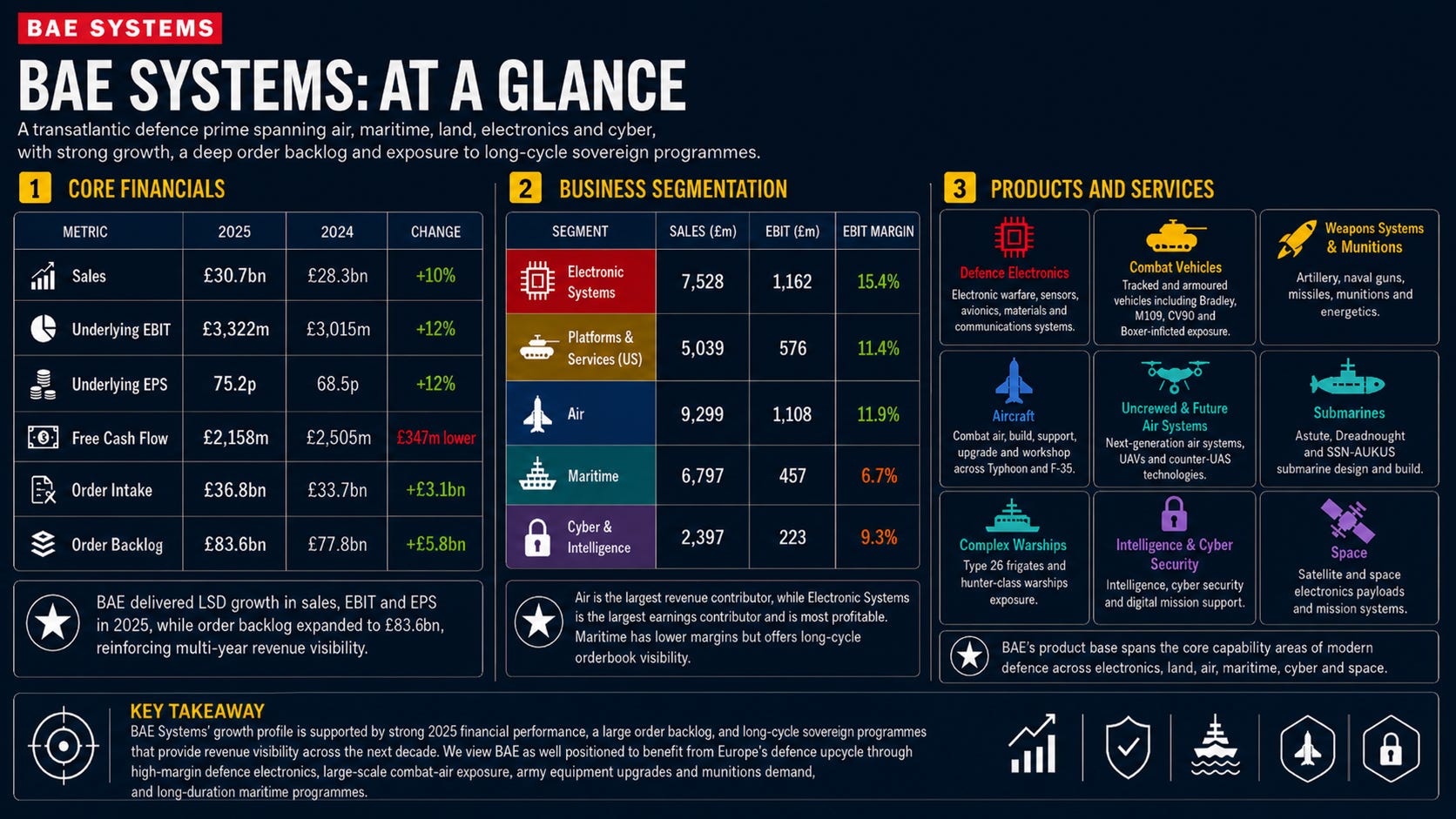

BAE’s moat is also anchored by incumbency. The global defence market is not a normal procurement market. Large programmes are tied to national security, classified systems, export controls, sovereign industrial capacity, specialist engineering depth and trusted relationships with a country’s Ministry of Defence (MoD). Once contractors are embedded in production lines for key defence technologies, switching become difficult because it introduces delivery risk, security risk and operational risk. This is visible in the structure of UK MoD budget. BAE was the largest private-sector MoD supplier in 2024/25, receiving £6.7bn, equivalent to 16.3% of total MoD expenditure. Around 91% of BAE’s 2024/25 MoD expenditure came through non-competitive routes, reflecting limited alternatives, high switching costs and the sovereign nature of its core programmes.

BAE reports through five core businesses: Electronic Systems, Platforms & Services, Air, Maritime, and Cyber & Intelligence. Its portfolio is diversified across every major military domain: Air, Land, Sea, Space, Cyber and Digital. This matters because BAE is not dependent on a single platform cycle, but sits across the areas where UK, US and allied defence spending is most likely to rise. The group operates with a 10.8% EBIT margin and has delivered a 5-year EBIT CAGR of 10.3%. Electronic Systems is the group’s most profitable business, while Platforms & Services has delivered the strongest EBIT growth driven by activities in the US. In our view, the profit mix should continue to be driven by defence electronics (Electronics Systems), ammunition (Platform & Services), missile defence (Air), submarines (Marine) and cyber defence.

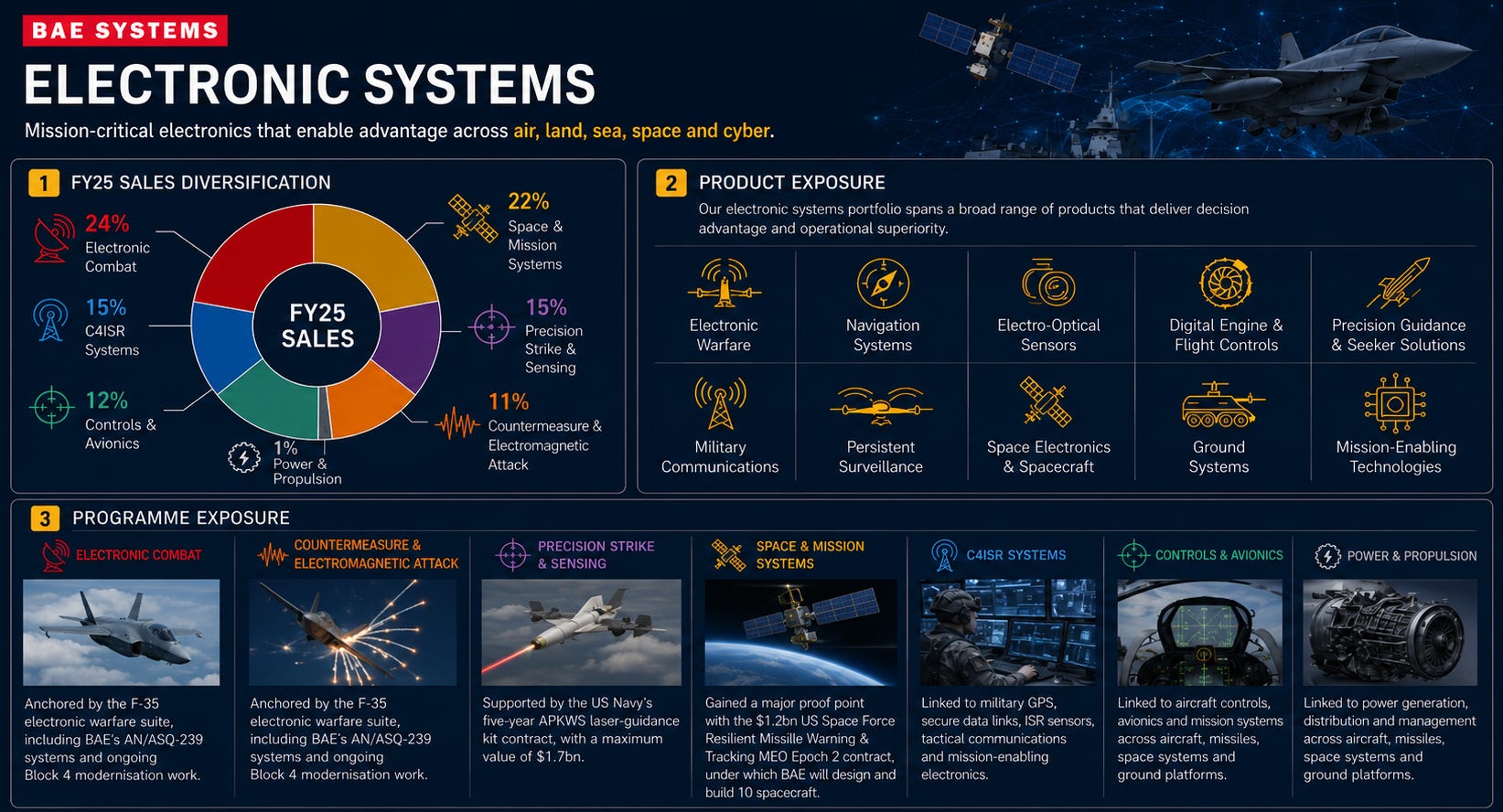

3.1 Electronic Systems — 25% Sales, 35% EBIT

Electronic Systems comprises BAE’s US- and UK-based electronic systems activities and the US-based Space & Mission Systems (SMS) business. It provides electronic warfare, sensors, precision guidance, C4ISR, space electronics, avionics, secure communications and mission-enabling technologies. The business contributes 25% of group sales and 35% of EBIT, making it BAE’s largest earnings contributor and highest margin business. It generates a 15.5% EBIT margin and has delivered a 5-year EBIT CAGR of 11.5% . In our view, Electronic Systems serves as the “picks and shovels” that support the functioning of all formats of defence equipment. Its electronics are embedded across aircraft, missiles, ships, satellites, vehicles, command networks and autonomous systems, making growth less dependent on any single platform cycle and more exposed to the broader digitisation of warfare.

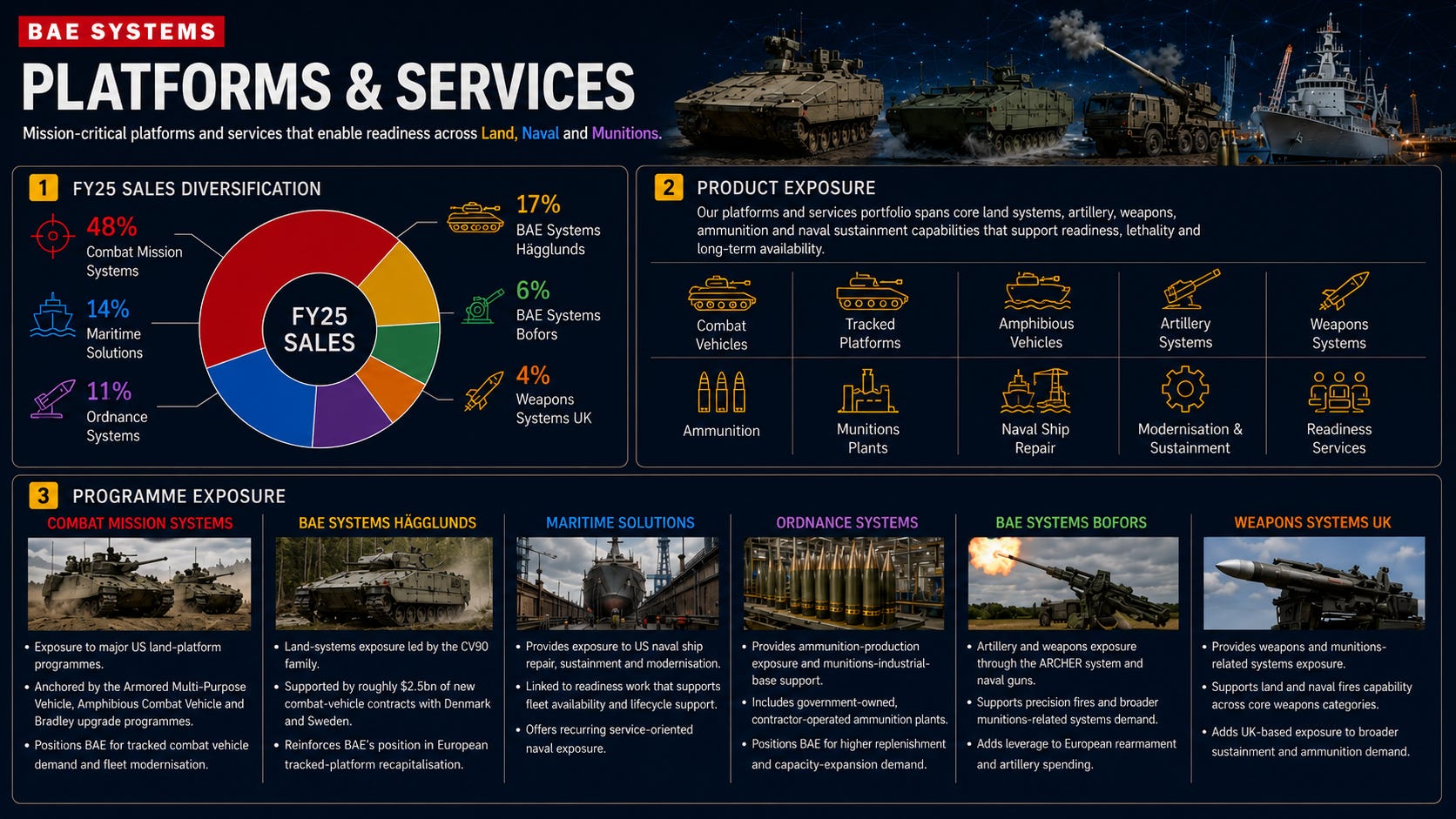

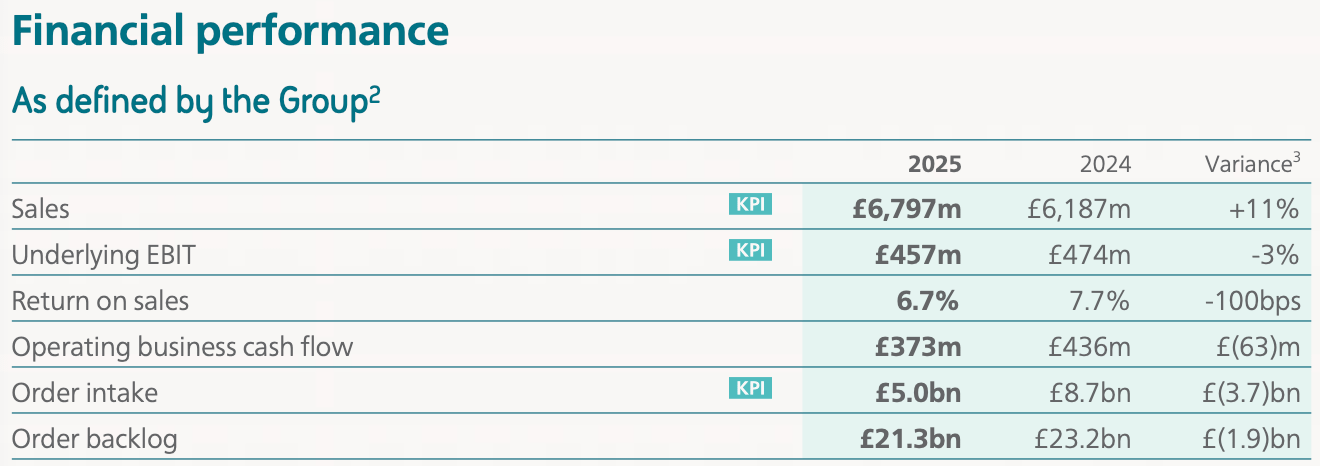

3.2 Platforms & Services — 16% Sales, 17% EBIT

Platforms & Services operates across the US (Combat Mission, Maritime, Ordnance), Sweden (Hägglunds and Bofors) and the UK (Weapon Systems). The business is primarily land-driven with some exposure to naval. Specifically, it manufactures and upgrades combat vehicles, weapons and munitions, while also providing naval ship repair, sustainment and support. The business contributes 16% of group sales and 17% of EBIT. It operates with an 11.4% EBIT margin and has delivered the strongest 5-year EBIT CAGR across the group at 24.8%. Over the past 3 years, Platforms & Services has been the strongest earnings-growth engine in the portfolio because it sits directly behind land readiness, munitions restocking and sustainment demand. The Ukraine war has structurally exposed Western undercapacity in ammunition, artillery, armoured vehicles and repair cycles, which should support elevated demand beyond a single budget year.

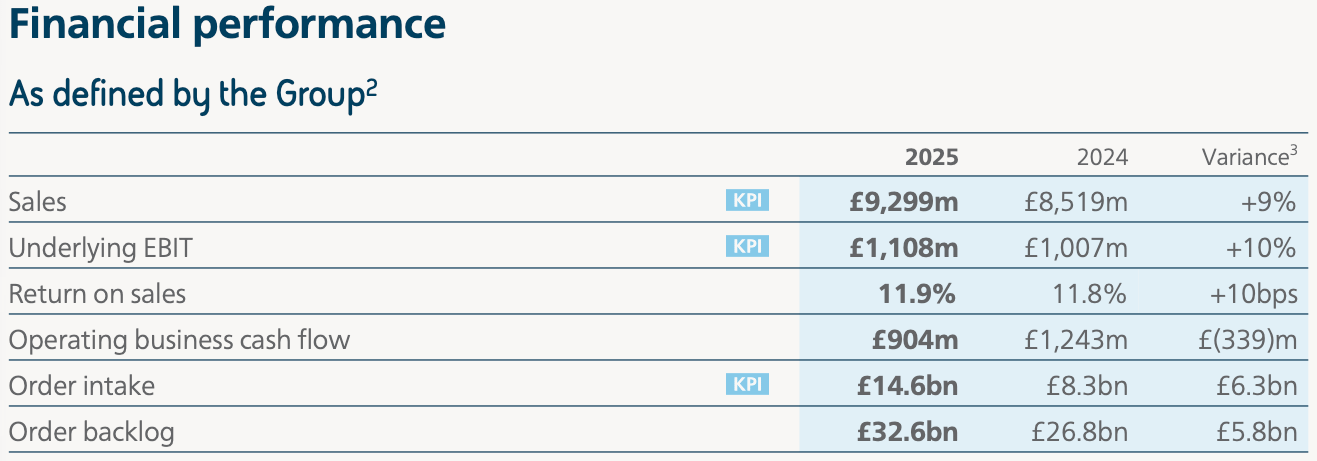

3.3 Air — 30% Sales, 33% EBIT

Air comprises BAE’s UK-based air build and support activities, European and international combat-air programmes (Typhoon, Hawk, Tornado), US programmes (F-35), Future Combat Air System development (GCAP via Edgewing), Saudi Arabia (Typhoon export and support) and its JV interests in MBDA (missiles). Air is BAE’s largest business by sales, contributing 30% of group sales and 33% of EBIT. It operates with an 11.9% EBIT margin but has delivered a lower 5-year EBIT CAGR at 4.0%. In our view, Air remains a core earnings anchor rather than the core near-term growth engine. The business benefits from long-duration combat air sustainment, missile exposure through MBDA and the strategic optionality of future combat air. Growth should improve if Typhoon support, missile demand and future air-system investment through GCAP and Edgewing convert into funded work packages.

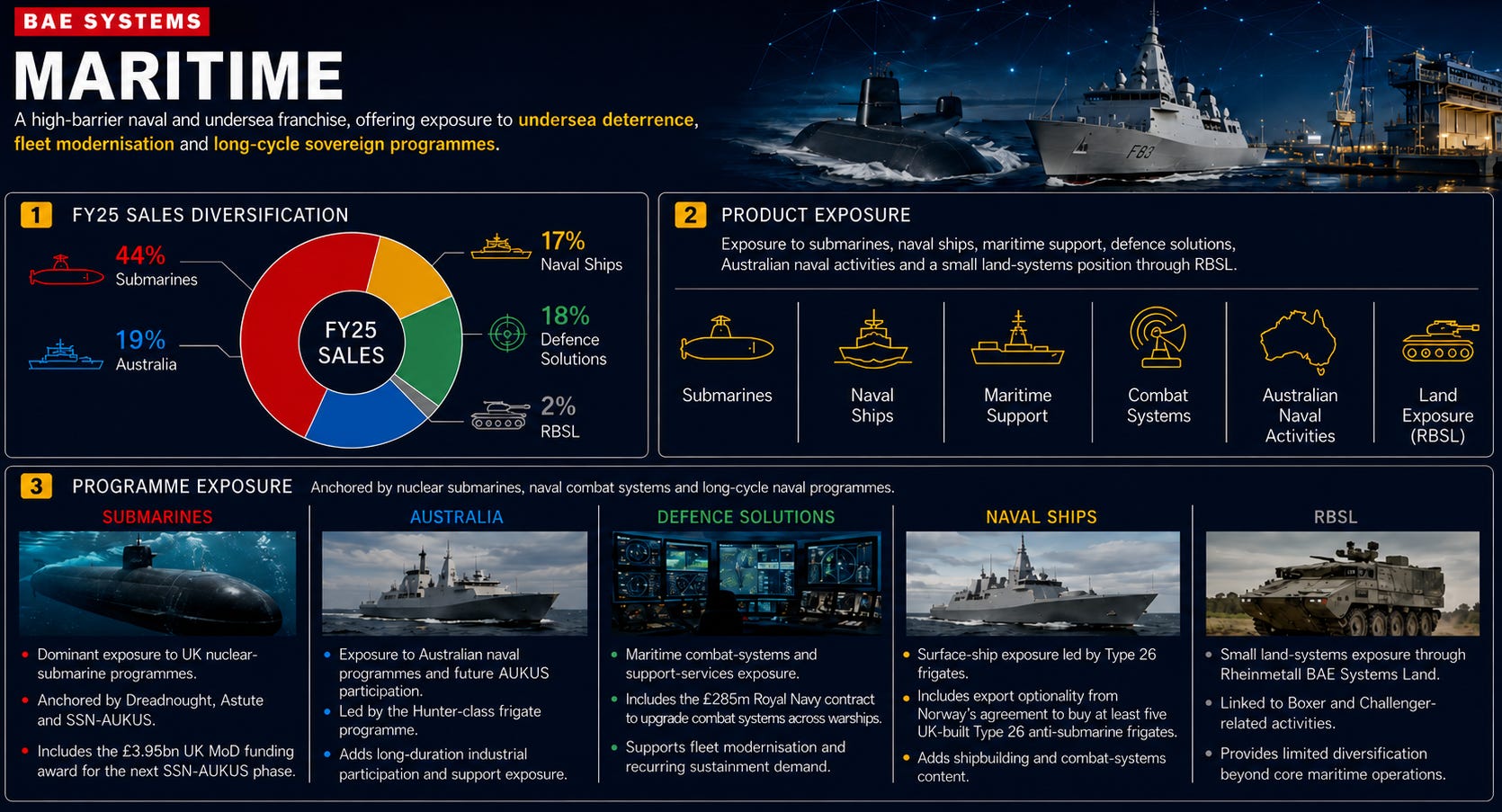

3.4 Maritime — 22% Sales, 14% EBIT

Maritime comprises BAE’s UK-based maritime and land activities, including ship build (Type 26 frigate), support (training and engineering services), major UK submarine build programmes (Astute-class, Dreadnought, SSN-AUKUS) and the group’s Australian business. The business contributes 22% of group sales and 14% of EBIT. It operates with a 6.7% EBIT margin, below the group average, but has delivered a 5-year EBIT CAGR of 10.4%. In our view, Maritime is BAE’s clearest sovereign capability business because it sits at the centre of UK nuclear deterrence, submarine production, naval shipbuilding and AUKUS-related industrial capacity. Growth visibility is strong because nuclear submarines and naval recapitalisation are multi-decade priorities with limited alternative suppliers.

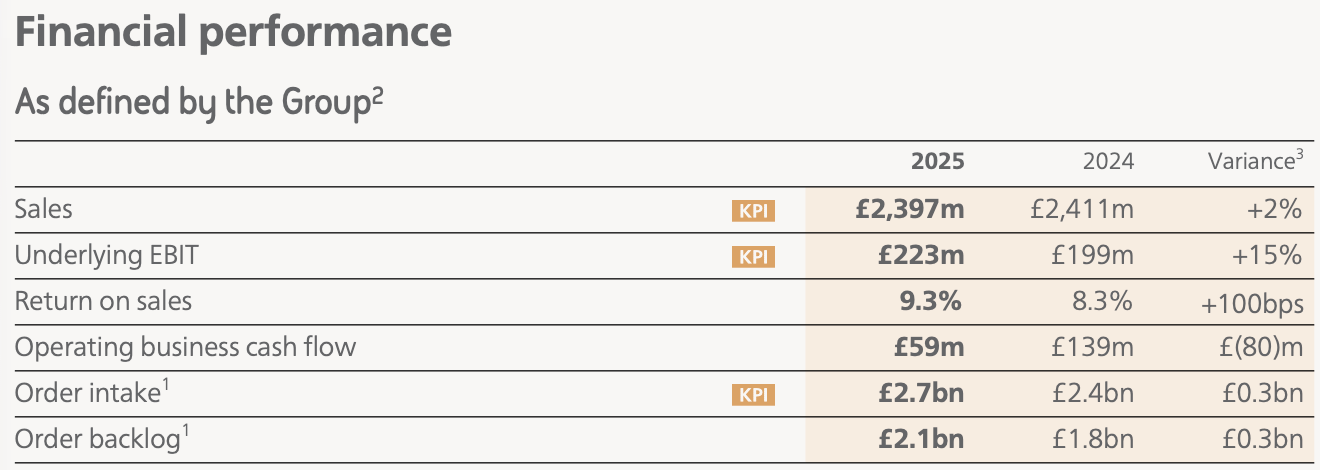

3.5 Cyber & Intelligence — 8% Sales, 7% EBIT

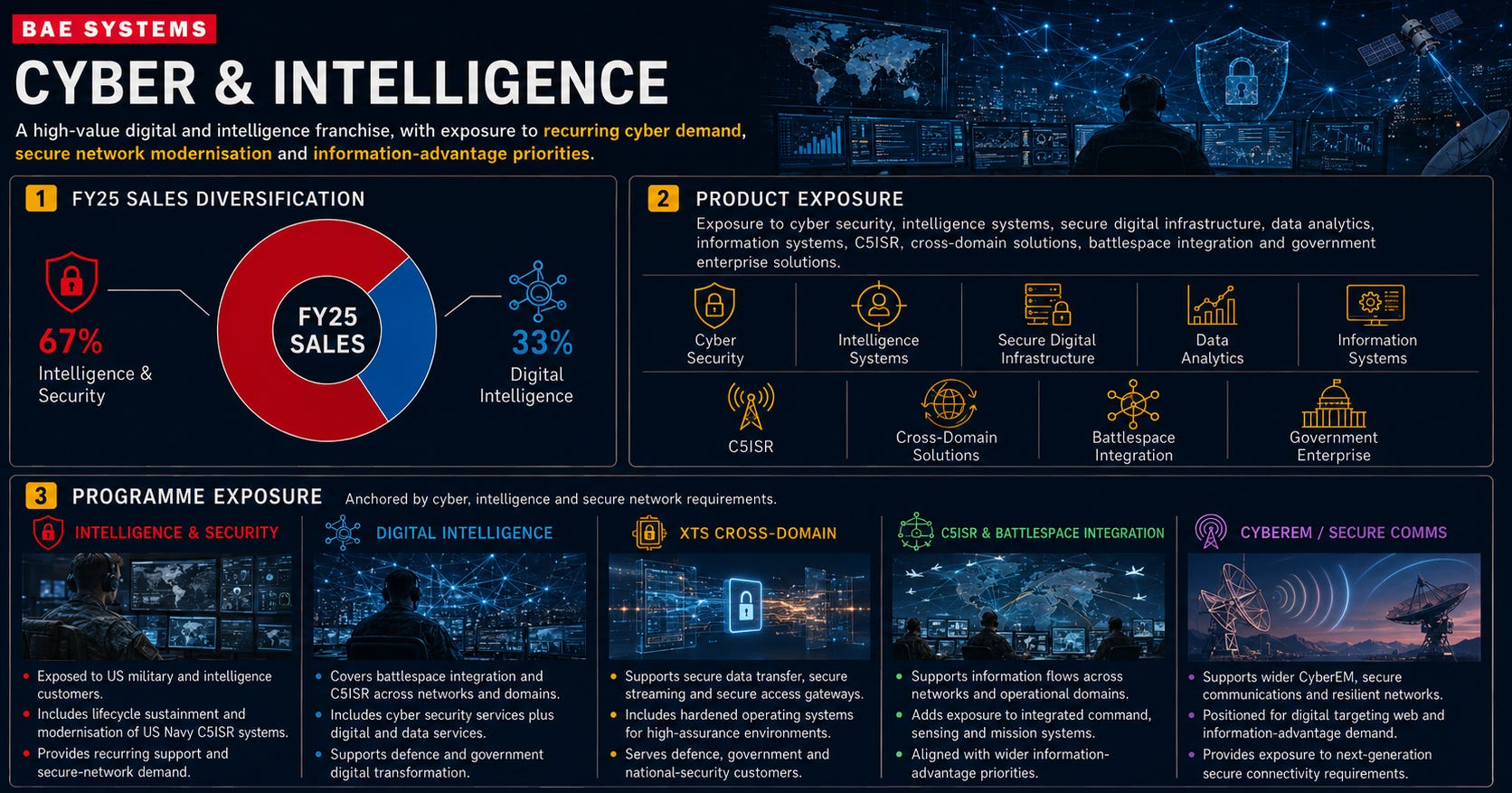

Cyber & Intelligence comprises the US-based Intelligence & Security business and the UK-based Digital Intelligence business. Intelligence & Security supports US defence and intelligence customers across Air & Space Force Solutions, Integrated Defence Solutions and Intelligence Solutions. These services cover mission systems, C5ISR integration, cyber, sustainment and intelligence-enabling tools. UK Digital Intelligence provides cyber, intelligence and secure digital capabilities for law enforcement, national security, central government, critical infrastructure, military and space customers.

The business contributes 8% of group sales and 7% of EBIT. It operates with a 9.3% EBIT margin and has delivered a 5-year EBIT CAGR of 10.6%. In our view, Cyber & Intelligence is strategically important because allied militaries are moving toward integrated, data-led and software-enabled warfare, where secure networks, intelligence processing and cross-domain information flows become core combat enablers. The growth runway is attractive, but the business remains smaller and more services-heavy than BAE’s platform franchises.

4. Strategic Priorities

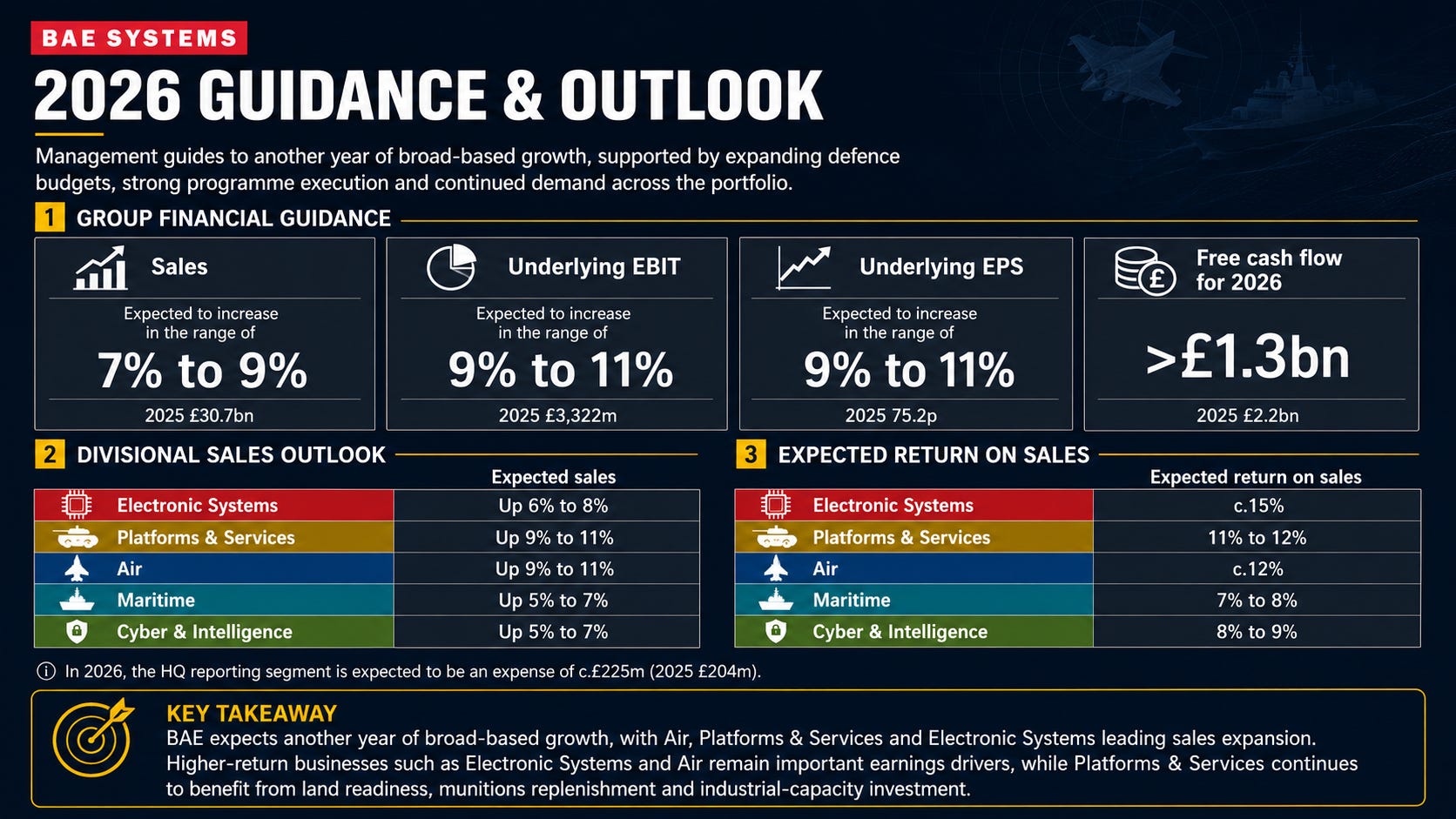

4.1 Forward guidance

We expect BAE to print another strong year of broad-based growth in 2026, with Electronic Systems, Platforms & Services and Air leading sales expansion. Higher-return businesses such as Electronic Systems and Air remain important earnings drivers, while Platforms & Services continues to benefit from munitions replenishment, land force modernisation and industrial capacity investment.

4.2 Divisional priorities

Electronic Systems has sustained strong operational performance across electronic warfare, precision-guided munitions, commercial avionics and space systems. The business benefited from continued demand for tactical space, mission payloads and aircraft survivability systems. Strategic order highlights include APKWS laser-guidance kits (£1.3bn), US Space Force Resilient Missile Warning & Tracking MEO Epoch 2 programme (£0.9bn), Long-Range Anti-Ship Missile radio-frequency sensors (£273m), Maritime Survivability Pod contracts (£190m, with £105m follow-on), FORGE C2 next-generation ground systems (£114m), and NOAA Space Weather Next spacecraft bus (£17m). Looking forward, Electronic Systems should remain a core growth engine. Demand is being driven by electronic warfare, precision strike, space resilience, missile warning, Golden Dome-related opportunities and next-generation power and propulsion systems. Execution risk sits around classified programme delivery, space integration and sustaining technology leadership.

Platforms & Services delivered strong operational performance, supported by healthy order backlog across combat vehicles, naval ship repair, munitions and artillery systems. The business continued to expand production capacity across US sites, while its Swedish Hägglunds unit transitioned from development to line-rate delivery and Ordnance progressed the Nitrocellulose Facility at Radford. Strategic order highlights include US Navy ship repair contracts (£800m), M109A7 Paladin self-propelled howitzers (£738m), CV90 MkIIIC vehicles for Denmark (£341m), US Marine Corps ACV contracts (£273m), and Bradley A4 upgrades (£71m). Bofors also secured Sweden’s first TRIDON Mk2 order and an ARCHER framework agreement. Looking forward, Platforms & Services should remain the clearest near-term growth engine. Demand is supported by munitions restocking, land readiness, European rearmament and US naval sustainment. Key risks are production bottlenecks, labour constraints, supply-chain pressure and normalisation of emergency restocking demand.

Air has continued to execute across Typhoon production, in-service support, US programmes and future combat-air development. Operational milestones included completion of Qatar Typhoon deliveries, F-35 rear-fuselage deliveries and launch of Edgewing with Leonardo and JAIEC for GCAP. Strategic order highlights include Typhoon package for Türkiye (£5.4bn), MBDA production orders across Aster, MRSAM and Exocet missile programmes (£1.8bn), European Typhoon major unit orders for Germany and Italy (£0.8bn), and ECRS Mk2 radar production for RAF Typhoon (£454m). Looking forward, Air remains a core earnings anchor. Growth is supported by Typhoon support, MBDA missile demand, F-35 workshare and GCAP. Key risks are UK funding clarity, international workshare, export timing, Saudi concentration and next-generation combat air execution.

Maritime continued to execute across long-cycle naval and submarine programmes. HMS Agamemnon was commissioned into the Royal Navy, Dreadnought construction advanced at Barrow, and Type 26 delivery progressed across UK and Australian yards. Operational performance also included RCODE (Real-time Combat System Open Data Enablers) availability support for the Royal Navy, Combat Management System modernisation and Australian sustainment work. Strategic order highlights include Canada’s Arctic Over-the-Horizon Radar support agreement, Irving Shipbuilding’s Canadian Surface Combatant design-services contract, ASC’s SSN-AUKUS mobilisation support contract, and PGZ’s 155mm munitions-factory partnership in Poland. Contract values were not disclosed. Looking forward, Maritime offers multi-decade visibility through Dreadnought, SSN-AUKUS, Type 26 and Australian naval programmes. The opportunity is highly strategic, but execution risk remains elevated given submarine complexity, labour constraints, infrastructure bottlenecks and margin pressure.

Cyber & Intelligence delivered resilient performance despite US government shutdown disruption and shifting US defence priorities. Intelligence & Security (US) continued to align with national security requirements, while Digital Intelligence (UK) progressed transformation work across law enforcement, defence and commercial customers. Operational highlights included electronic warfare and counter-UAS capability expansion through the Kirintec acquisition, Azalea low-earth-orbit satellite cluster work and the Bradley Fighting Vehicle training system development. Strategic order highlights include the US Air and Space Force Solutions Systems Engineering, Evaluation and Analysis Worldwide contract (£180m). Other contract values were not disclosed. Looking forward, Cyber & Intelligence should benefit from AI, autonomy, cyber, counter-UAS, digitisation and secure network demand. The key risks are services heavy revenue, talent competition, contract timing and weaker long-cycle visibility versus platforms, submarines or munitions.

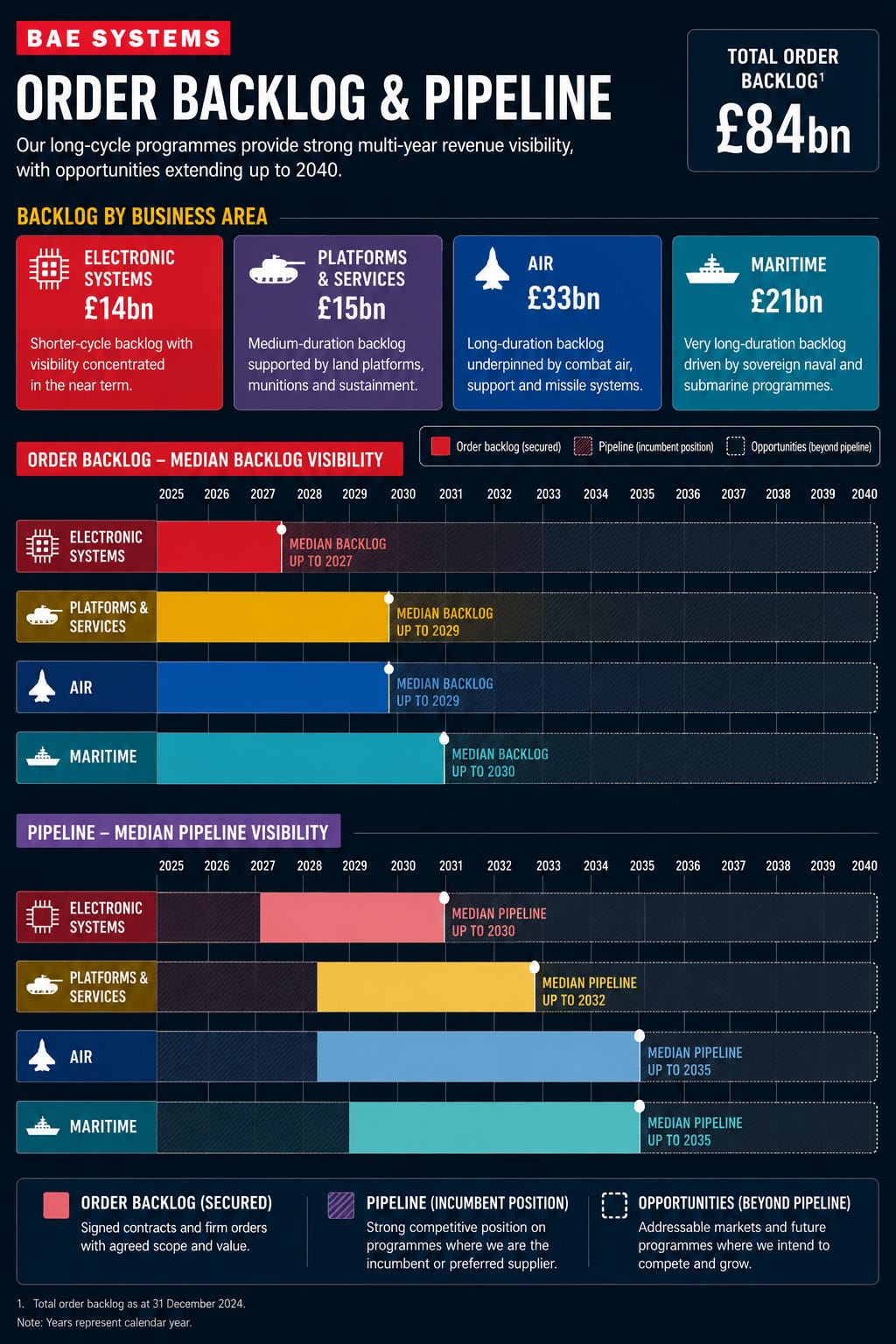

4.3 Order backlog and pipeline

We view BAE’s £84bn order backlog as a core pillar of the investment case, providing unusually strong multi-year revenue visibility across the portfolio. While highly profitable, Electronic Systems is a shorter-cycle business with backlog visibility to 2027 and pipeline visibility to 2030. We think this can be offset by recurring demand across electronic warfare, sensors, C4ISR and mission systems.

Platforms & Services and Air provide deeper secured visibility to 2029, supported by army equipment upgrades, munitions replenishment, combat air production, aircraft support and missile exposure. Maritime is the highest-quality backlog asset in our view, with secured visibility to 2030 and pipeline visibility to 2035, anchored by submarines, Type 26 and Australian naval programmes. Our read through is that BAE combines near-term revenue conversion in electronics and land systems with long-cycle visibility in Air and Maritime, creating a durable earnings base through the defence spending upcycle.

5. Governance considerations

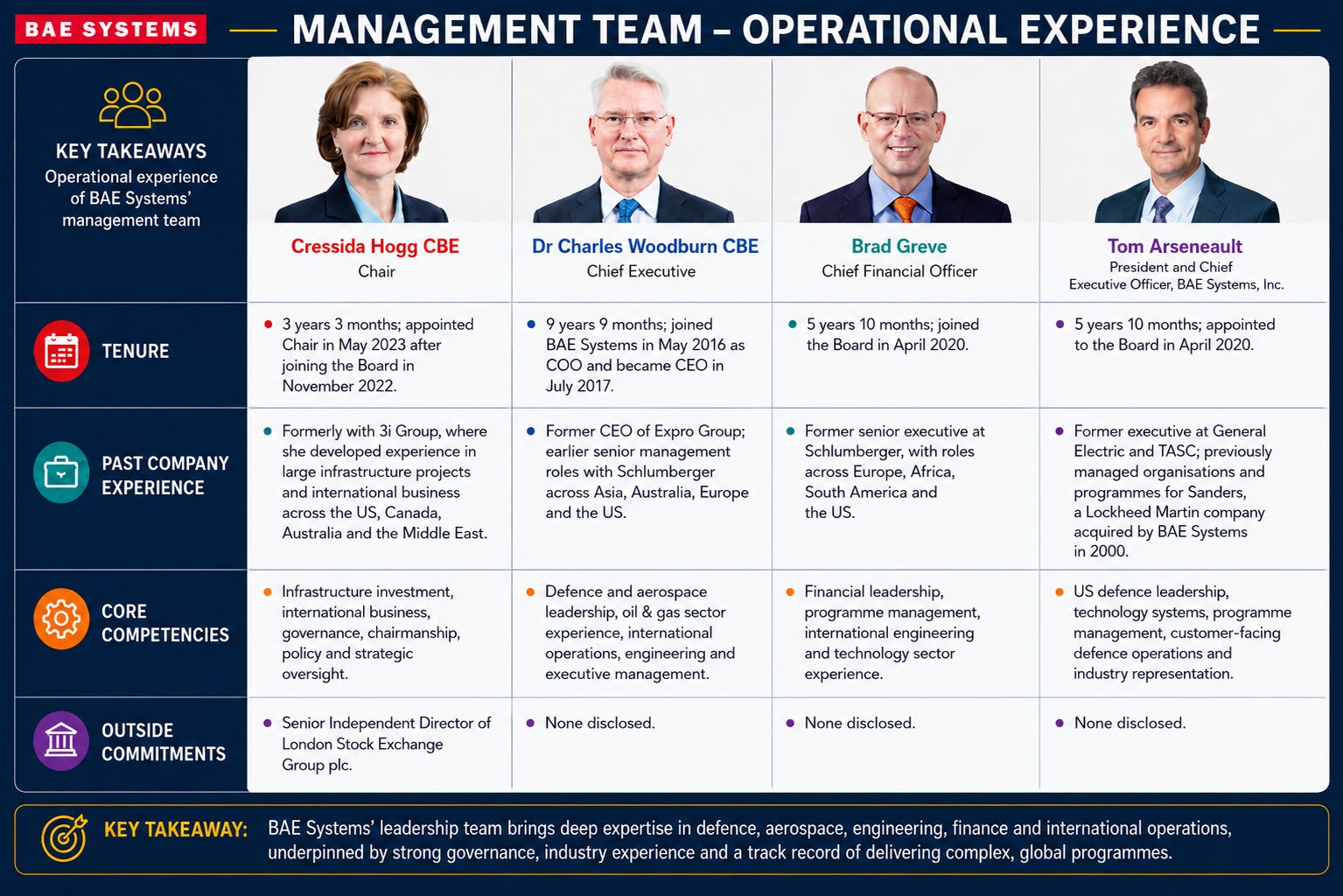

5.1 Management Team

BAE’s core leadership team brings a complementary mix of infrastructure, defence, engineering, finance and US defence-market experience. CEO Charles Woodburn brings deep engineering and international industrial experience, with prior senior roles at Schlumberger and direct leadership of BAE since 2017. CFO Brad Greve adds financial and operational experience from more than 30 years across global engineering and technology businesses. Tom Arseneault, CEO of BAE Systems, Inc., brings deep US defence market experience from senior roles across BAE’s US business and predecessor organisations, which is critical given the US is BAE’s largest sales market. We are also positive on management focus: Woodburn, Greve and Arseneault have no outside commitments on listed companies, while Hogg’s main listed commitment is as Senior Independent Director of LSEG.

5.2 Board oversight

We also think the broader BAE’s Board has a strong mix of skills for a long-cycle defence business. The deepest areas of experience are international business/commercial, company leadership, long-term contracting, engineering/science/technology, board experience and risk management. This matters because BAE’s value creation depends on programme execution, government relationships, complex contracting, technology leadership and risk control. Board attendance also appears strong. Most directors attended all scheduled Board meetings, with 7/7 attendance shown across the core Board. Committee attendance was also generally high across Audit and Risk, ESG, Innovation and Technology, Nominations and Remuneration. This supports a positive governance read-through.

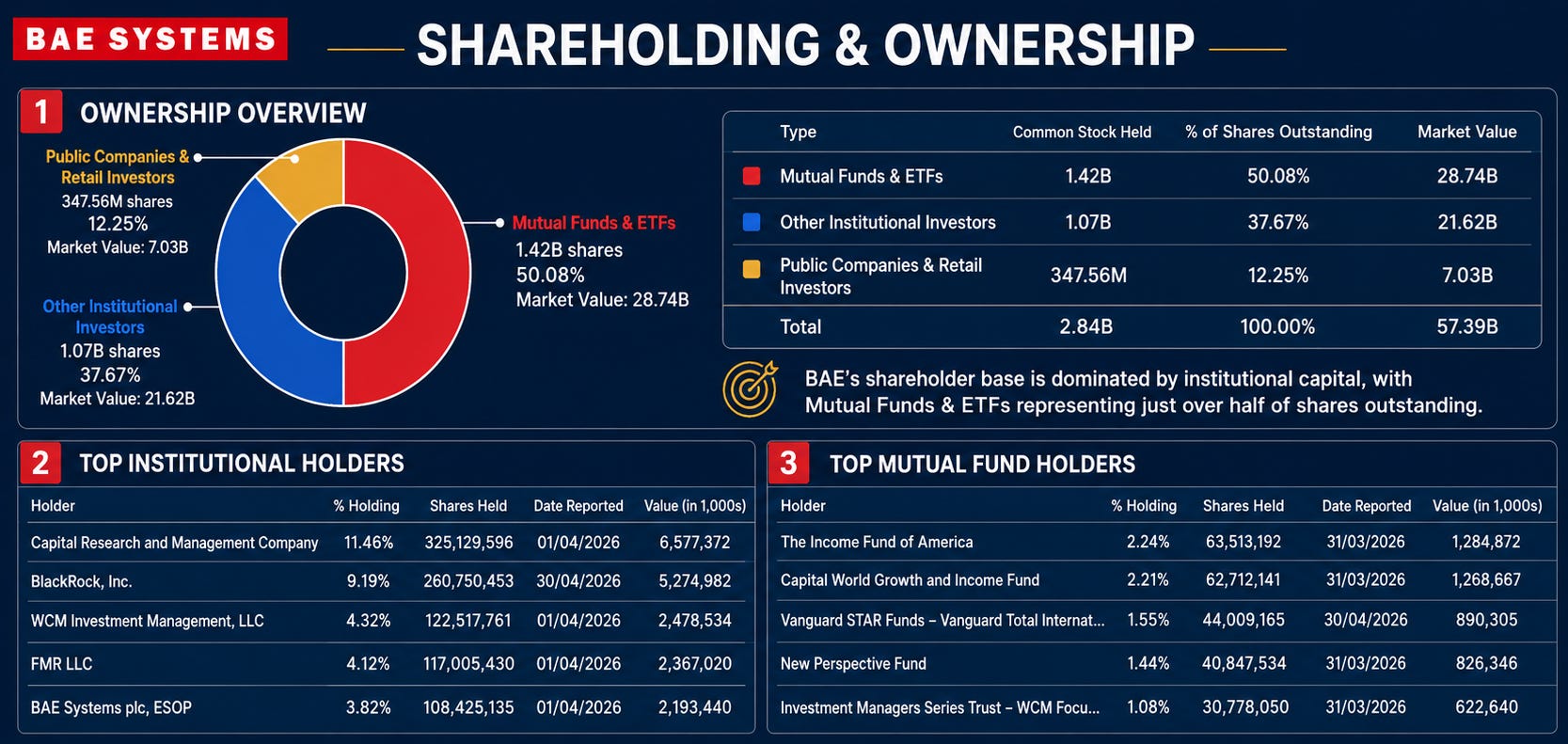

5.3 Shareholding and ownership

BAE’s shareholder base is highly institutional. In our view, this ownership structure is supportive because the shareholder base is dominated by institutional capital rather than strategic, activist or state shareholders. While the UK government does not appear as an ordinary equity holder, BAE should not be viewed as a normal public company with no state influence. The UK government holds a Special Share, or “golden share”, giving it consent rights over certain strategic matters, including foreign ownership limits and British control requirements. We think this allows the company to maintain independence in public markets while protecting BAE’s sovereign defence role.

5.4 Capital allocation

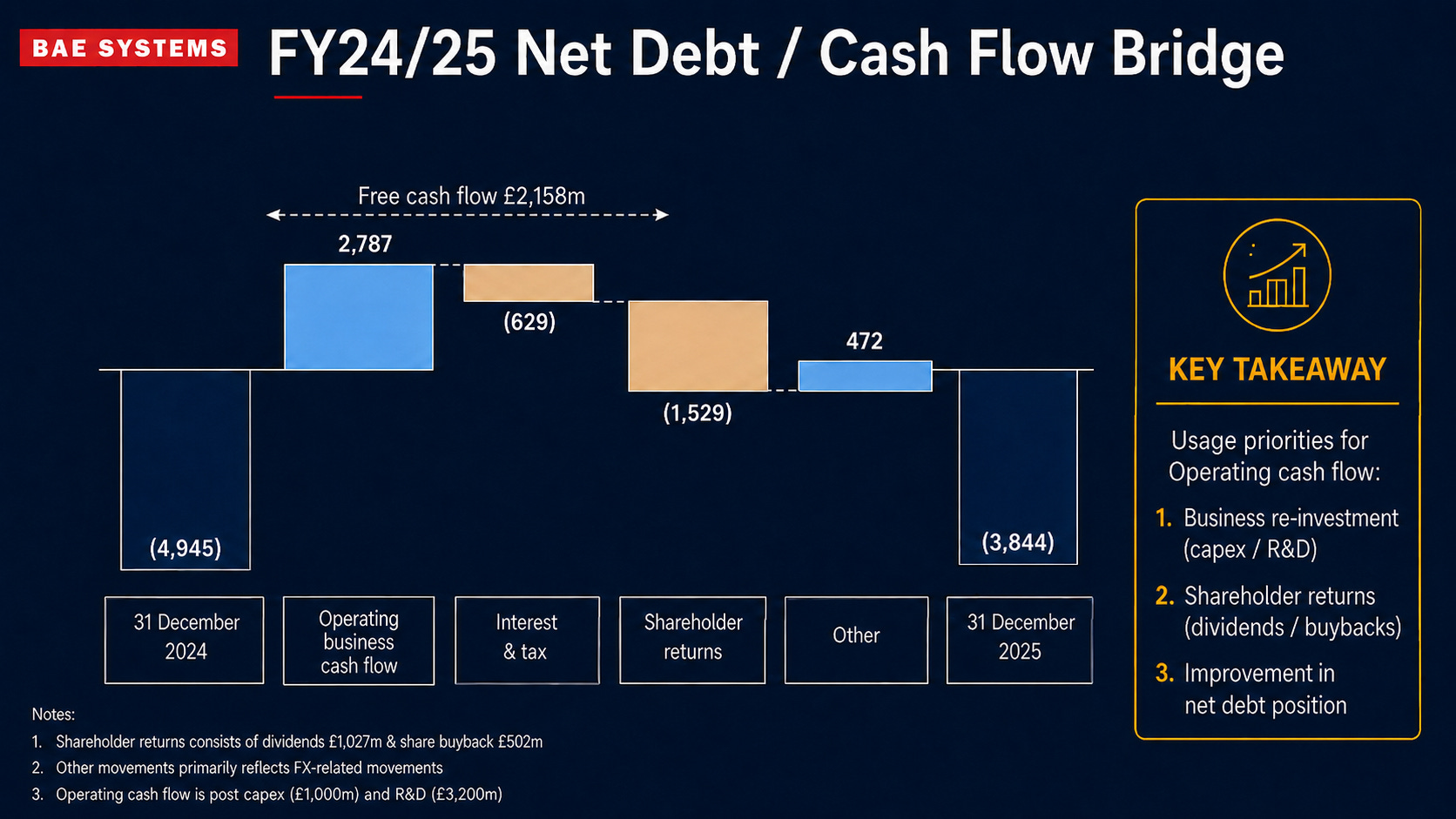

We think BAE’s capital allocation framework is disciplined, balanced and well suited to a long-cycle defence upturn. Management is prioritising reinvestment in the business to protect programme execution, sustain technological leadership and preserve balance-sheet strength. Against 2025 sales of £30.7bn, BAE invested £3.2bn in R&D (10.4% of sales), £1.0bn in capex (3.3% of sales), and supported 6,800 apprentices, undergraduates and graduates in the UK. We think recruiting graduates has long-term strategic benefits as this strengthens employee retention on long-duration programmes. It concurrently reduces reliance on mid-career hiring, where sector switching can be limited by specialisation and security clearance requirements.

We also think BAE has enough cash generation to balance capex with shareholder returns. Free cash flow was £2.158bn (7.0% of sales). Total dividend per share was 36.3p (53% payout), against EPS of 68.8p. The group invested £6.0bn in M&A from 2020 to 2025 (4% p.a. of 2025 sales), including the £4.4bn Ball Aerospace acquisition, while repurchasing £502m of shares (9% of 2024 share capital). Remainder of the capital generated from FCF trickled down to the net debt profile, with 2025 Net Debt / EBITDA at slightly under 1x. In our view, the balance of priorities here creates an attractive capital allocation mix: fund organic growth first, pursue capability-led M&A, and return surplus capital to shareholders. By maintaining disciplined investment in production capacity, engineering capability and technology development, BAE is positioning itself ahead of potential industry bottlenecks as defence demand accelerates.

5.5 Stakeholder management

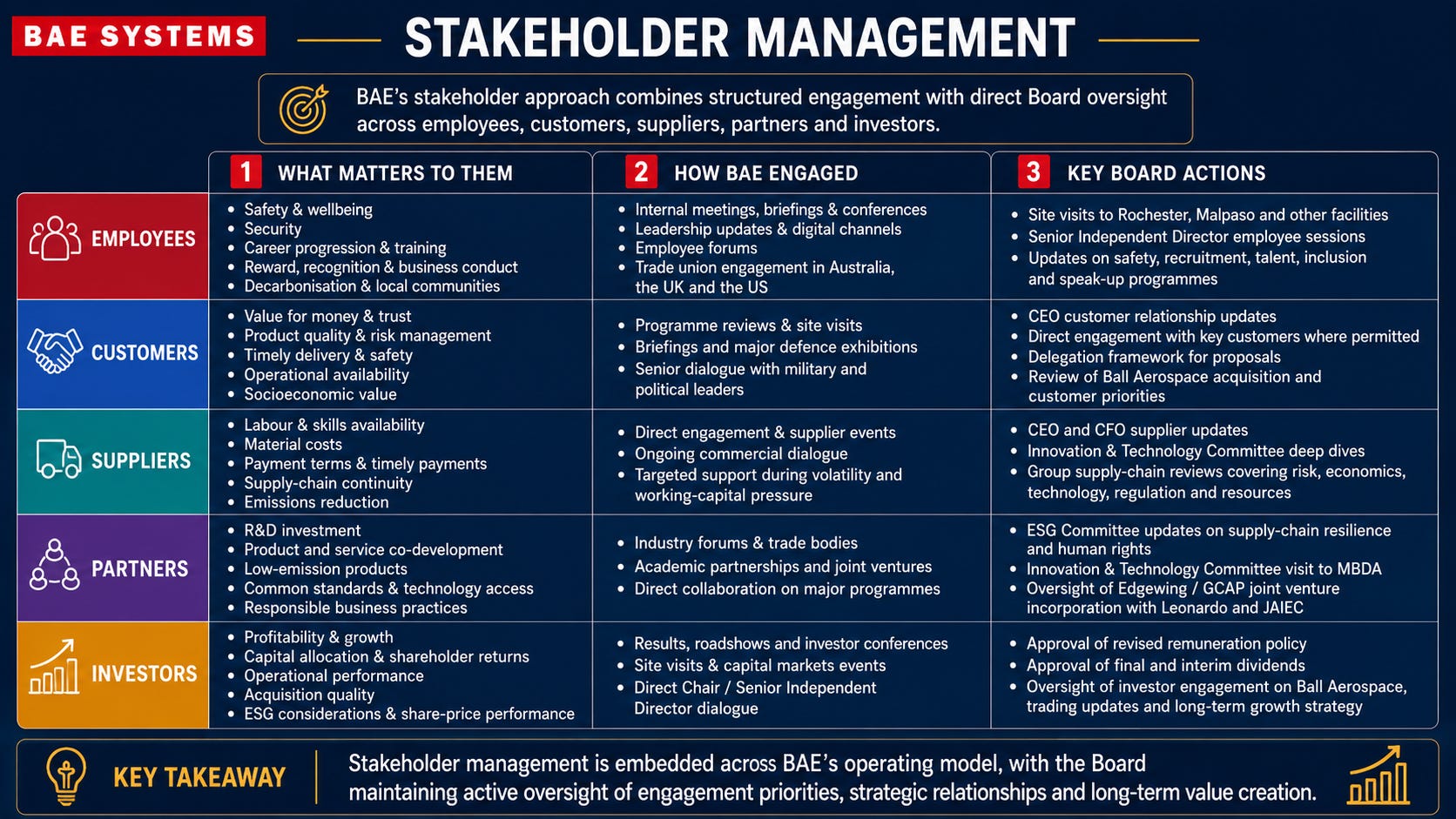

BAE’s stakeholder engagement model is built around maintaining trust, delivery credibility and long-term alignment. Employees are engaged on safety, wellbeing, skills and inclusion through leadership updates, forums, site visits and trade union dialogue. Customers, primarily governments and defence end-users, are engaged through programme reviews, site visits, senior meetings and defence exhibitions. Suppliers are engaged through direct dialogue and support on continuity, cost and resilience. Partners are engaged through joint ventures, industry forums and programme collaboration, including GCAP / Edgewing and MBDA. Investors are engaged through results, roadshows, site visits and capital markets events.

This article is the first of a two‑part series on BAE Systems. In the follow‑up note, we will focus on the company’s financial profile, forward outlook, and investment case.

Author’s note: This material and/or its contents are current at the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the written consent of the Author. Any view expressed herein is from the Author, is based on available information, and are subject to change without notice. While any third-party data used is considered reliable, its accuracy is not guaranteed. Forward-looking statements should not be considered as guarantees or predictions of future events. Past results are not a reliable indicator of future results. The Author assumes no duty to update any information in this material if any such information changes.

Very interesting info here! Keep up the good work. I’m more in the personal finance niche but it’s always interesting exploring different sectors within finance as a whole.