BAE Systems: Buy the DIP?

UK politics creates timing risk, while Burnham’s defence stance could increase funding upside if he can manage MoD and Treasury tensions

Summary:

Leadership change in the UK Government might increase the risk of a short-term delay to the Defence Investment Plan, but should not materially reduce the likelihood of publication. To us, the more important question is whether new leadership will revisit the plan’s funding and spending assumptions. For BAE Systems, we think the principal risk is timing rather than direction. The UK still needs to rebuild military capability, strengthen readiness and provide industry with a clearer procurement roadmap. A published DIP should therefore remove an important overhang on BAE and other UK defence stocks by providing investors with better visibility into programme priorities, procurement timelines and the allocation of incremental defence spending. We view recent weakness in the shares as an attractive entry point if the DIP provides clarity on funded orders and medium-term programme visibility.

This article is a follow-up on BAE Systems. For a more detailed analysis, refer to our deep dive and investment thesis here.

Table of Contents

DIP Implications

1.1 Funding size and timing

1.2 Programme approval riskUK leadership transition

2.1 DIP timing dispute

2.2 Andy Burnham’s defence stance

2.3 MoD- Treasury tensionsDivisional sales exposure

3.1 Air

3.2 Maritime

3.3 Platform and services

3.4 Cyber and intelligenceInvestment implications

4.1 Order intake and backlog conversion

4.2 Pipeline at risk

4.3 Margin and cash flow

4.4 Key risks4.5 Recommendation

1. DIP implications

1.1 Funding size and timing

The UK Defence Investment Plan is the key near-term policy catalyst for BAE Systems as it should translate the 2025 Strategic Defence Review into a funded procurement and capability roadmap. The market understands that UK defence spending is already moving higher, so the real question is whether the final plan is sufficiently large, specific and front-loaded to support major defence programmes. Leadership change increases the risk of short-term delay and could push contract awards into the next administration, but we do not think it changes the strategic rationale for higher UK defence spending. For BAE, a smaller or delayed plan would not break the investment case, but it could slow the pace at which defence ambition turns into funded orders. Furthermore, BAE’s UK exposed revenues are approximately 27% for FY2025, suggesting that the bulk of our thesis still hinges on global defence spending ex-UK coming through.

1.2 Programme approval risk and capability priorities

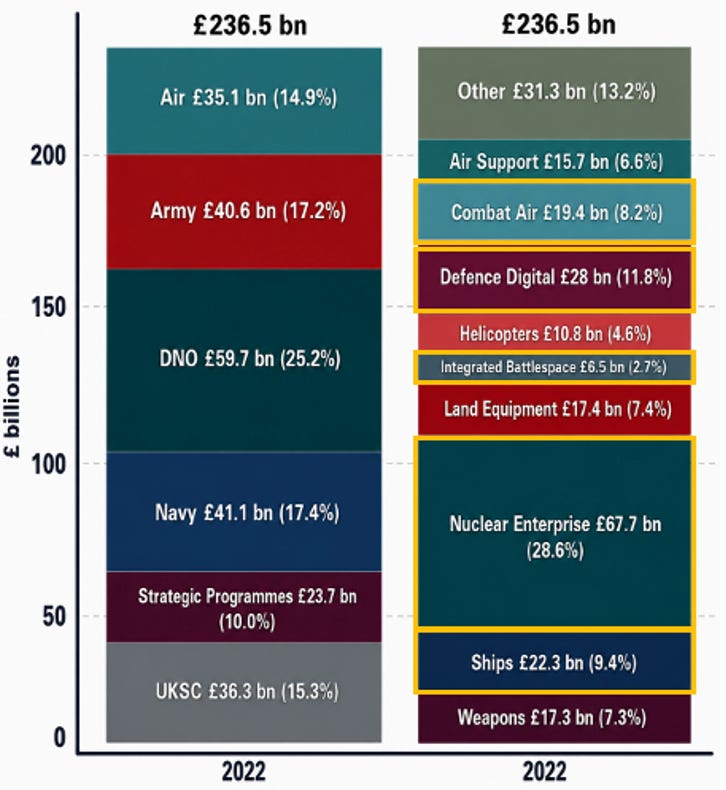

The main risk for UK defence equities is timing, not direction. If the funding envelope is constrained, the UK cannot fund every priority at the same pace, making the DIP a programme selection exercise. For BAE, the key capability areas are clear: GCAP and combat air support the Air division, AUKUS and submarines support Maritime, munitions and sustainment support Platforms & Services, while sensors, electronic warfare and mission systems support Electronic Systems. Spending projections for the UK MoD are laid out below based on 2022/23 fiscal year estimates for a period of 10 years.

2. UK leadership transition

2.1 DIP timing dispute

The UK leadership transition has become directly relevant to the Defence Investment Plan. Sir Keir Starmer is still expected to publish the DIP ahead of the NATO summit in Turkey on 7 July, but Andy Burnham’s allies argue that an outgoing Prime Minister should not lock in a major defence-spending plan weeks before leaving office. For BAE, this creates timing risk rather than direction risk. Should the publication date slip, or the plan be reopened under Burnham, or contract awards could move into the next administration - the UK still needs a formal defence investment framework.

2.2 Andy Burnham’s defence stance

Burnham’s reported position is important because he does not appear to be arguing for a weaker defence agenda. His team has told Labour MPs that he wants to give the MoD more than the £13.5bn currently offered in the DIP, while John Healey’s support suggests the funding debate could be reopened on more favourable terms for defence. The key question is therefore whether Burnham pushes the settlement closer to what defence leaders had sought. For BAE, a larger or more front-loaded DIP would improve visibility for GCAP, AUKUS, submarines, munitions, missiles, electronics and sustainment.

2.3 MoD–Treasury tensions

The leadership dispute also highlights the deeper tension between the MoD and the Treasury. The MoD wants more funding to address readiness gaps, rebuild stockpiles and protect major programmes, while the Treasury remains focused on affordability and sequencing. Dan Jarvis has already signalled that he has found more funding, with reports suggesting other departments may be asked to make cuts to reallocate money to defence. For BAE, the key message is that political uncertainty may delay programme approvals, but it does not weaken UK strategic demand for the group’s capabilities.

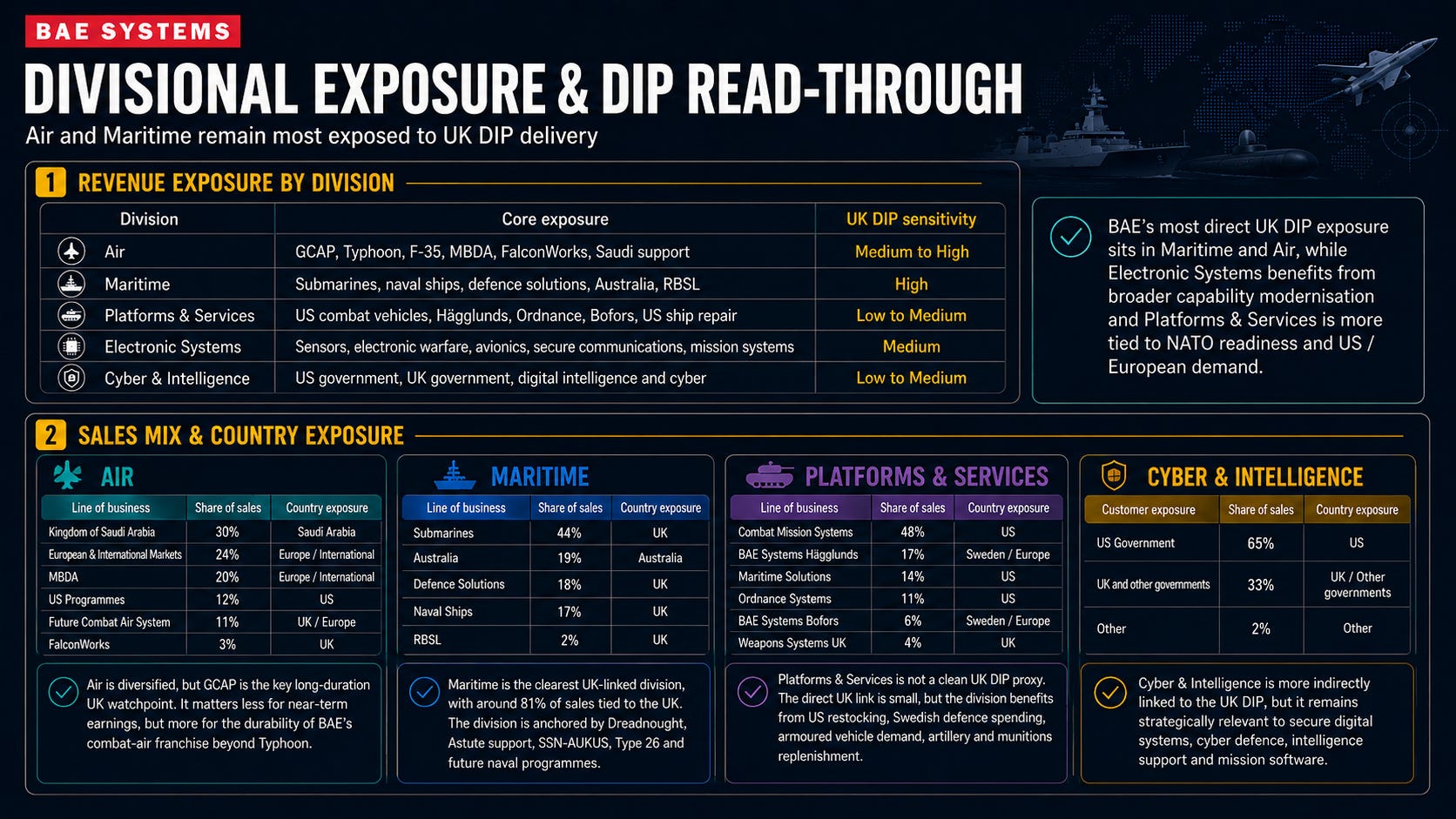

3. Divisional sales exposure

3.1 Air

BAE’s Air division is exposed to GCAP, Typhoon support and upgrades, F-35 workshare, MBDA missile activity and FalconWorks. The division is not just a UK combat-air business. Its revenue base is diversified across Saudi Arabia, Europe and international markets, missile exposure through MBDA, US programmes, future combat air and advanced technology development.

GCAP is the main long-duration watchpoint. While it is not the most important near-term earnings driver, it’s earnings trajectory matters for the durability of BAE’s combat-air franchise beyond Typhoon. The DIP should help investors assess whether the UK remains fully committed to GCAP’s funding path, development timeline and industrial role. If the plan provides clear support, it should improve confidence in BAE’s long-term Air pipeline. If the plan is delayed, reduced or back-loaded, GCAP could remain a source of timing uncertainty.

3.2 Maritime

BAE’s Maritime division is mainly a UK-exposed submarine and naval-systems business, with Australia as the main non-UK revenue contributor. Its sales are led by Submarines, followed by Australia, Defence Solutions, Naval Ships and RBSL.

This makes Maritime one of the clearest read-throughs to UK defence funding. Around 81% of the division is UK-linked, with exposure to Dreadnought, Astute support, SSN-AUKUS, Type 26 and future naval programmes. The division should remain highly protected because submarines, nuclear deterrence and undersea capability sit at the centre of UK defence strategy, but investors should still watch delivery discipline, labour capacity and cost control.

3.3 Platforms & Services

BAE’s Platforms & Services division is mostly non-UK exposed, with revenue led by Combat Mission Systems, Hägglunds, Maritime Solutions, Ordnance Systems and Bofors. The only directly UK-exposed line is Weapons Systems UK, which represents a small share of divisional sales at 4%.

This means Platforms & Services is least exposed to the risks from the UK DIP. The division still benefits from the broader NATO readiness cycle, including US restocking, Swedish defence spending and demand for armoured vehicles, artillery, naval weapons and munitions.

3.4 Cyber & Intelligence

BAE’s Cyber & Intelligence division is mainly exposed to government customers, with the US Government making up the largest share of sales. This means the division is less directly exposed to the UK DIP than Maritime or Air, but it remains relevant to broader digital defence, intelligence and secure systems demand.

The division is smaller than Air, Maritime or Electronic Systems, but it adds strategic depth to BAE’s portfolio. Its exposure to secure digital systems, intelligence support, cyber defence, data infrastructure and mission software should benefit from the broader shift toward connected defence, digital command and intelligence-led warfare. For the DIP, the read-through is less direct and material.

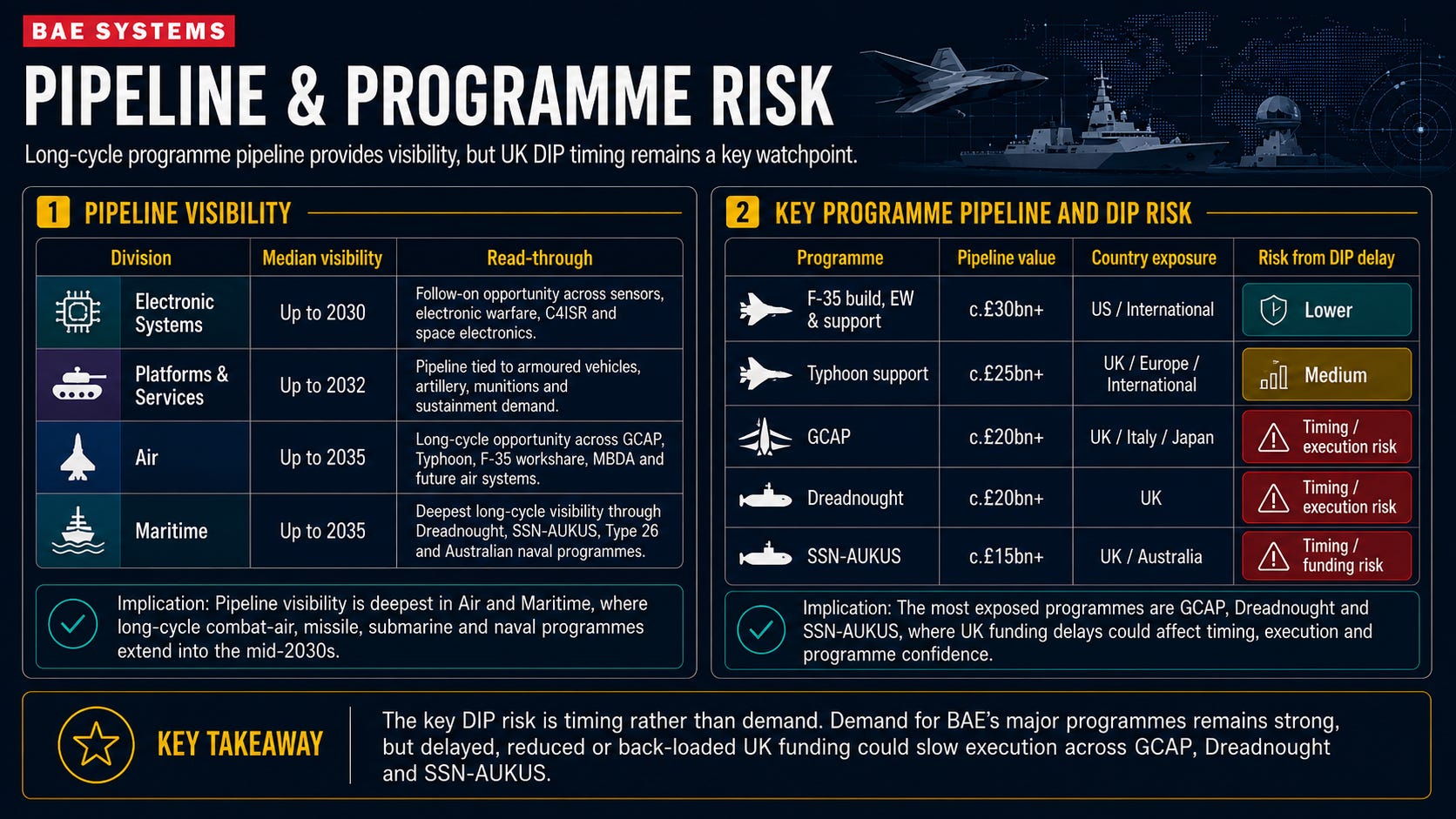

4. Investment implications

4.1 Order intake and backlog conversion

The DIP matters because it should turn defence policy into funded orders. BAE already has strong backlog visibility, but the next leg of the thesis depends on new programme commitments and order conversion. Investors will look for evidence that the DIP supports GCAP, AUKUS, submarines, munitions, missiles, electronic systems and sustainment. A clear plan should reduce policy uncertainty and support order intake. A delay or funding reassessment could push contract awards further out, even if the medium-term direction remains positive. For BAE, the key question is not whether demand exists. It is whether the UK can move from ambition to procurement.

4.2 Pipeline at risk

The key risk from the DIP is not near-term revenue, but long-term pipeline visibility. BAE has disclosed a pipeline of around £180bn, equivalent to roughly 9x sales, with major long-duration programmes running into 2035 and beyond. The directly UK-exposed programmes within this pipeline are Dreadnought, SSN-AUKUS and GCAP. Together, these represent around £55bn+ of potential programme value, or roughly 31% of BAE’s disclosed pipeline. This is the part of the pipeline most exposed to UK funding clarity, programme approvals and the final shape of the DIP.

This does not mean 31% of the pipeline is at risk of cancellation. Dreadnought and SSN-AUKUS are strategically protected because they sit at the centre of the UK’s nuclear deterrent and undersea strategy. GCAP is also strategically important, but more exposed to funding phasing and political commitment. The real risk is therefore delay, not demand destruction. If the DIP is delayed, underfunded or reopened under new leadership, BAE could face slower order conversion across these programmes, even if the medium-term strategic case remains intact.

4.3 Margin and cash flow

BAE’s margin and cash flow read-through depend on execution, programme phasing and working-capital discipline. Higher defence demand is positive, but it does not automatically translate into higher cash flow. Large programmes can require upfront investment, working-capital build and supply-chain capacity. Submarine work in particular is strategically protected but execution-heavy.

The DIP should therefore be assessed not only on order value, but also on programme mix. Near-term munitions, sustainment and electronics work could support cleaner conversion. Long-cycle platform work supports duration, but may carry more execution and cash-flow timing risk. For investors, the quality of growth matters as much as the quantity of growth.

4.4 Key risks to monitor

The main risks are DIP publication delay, a funding envelope that remains closer to the lower level being debated, back-loaded spending, GCAP funding stretch, AUKUS and submarine execution pressure, weaker-than-expected munitions and air-defence orders, Type 83 slippage, supply-chain bottlenecks and rising working-capital needs.

These risks do not change BAE’s strategic relevance, but they matter for timing, revenue conversion and investor confidence. The market will likely look through some political noise if the DIP confirms the direction of spending. But if publication slips or the plan lacks programme-level detail, the stock could remain caught between a strong long-term thesis and weaker near-term visibility.

4.5 Recommendation

For BAE Systems, the principal risk is timing rather than direction. The UK political backdrop will remain uncertain with abundant fiscal constraints in the medium term. That being said, the direction of travel for UK defence spending is still higher, and the institutional need for a formal investment plan remains intact. The company is exposed to the UK’s most protected capability areas: GCAP, AUKUS, submarines, munitions, missiles, electronic systems and sustainment. A published DIP should remove an important overhang and support a re-rating of UK defence-exposed stocks.

Our view is that investors should “buy the DIP” if the publication provides clearer visibility on programme priorities, procurement timelines and incremental defence spending. More than 70% of the company’s revenues are still driven by global defence spending tailwinds, excluding the UK. We believe current valuations price in the risk of the DIP releases, and recommend an add at prices below GBX 1,800.

This article is a follow-up on BAE Systems. For a more detailed analysis, refer to our deep dive and investment thesis here.

Author’s note: This material and/or its contents are current at the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the written consent of the Author. Any view expressed herein is from the Author, is based on available information, and are subject to change without notice. While any third-party data used is considered reliable, its accuracy is not guaranteed. Forward-looking statements should not be considered as guarantees or predictions of future events. Past results are not a reliable indicator of future results. The Author assumes no duty to update any information in this material if any such information changes.

Your publication has definitely earned a spot in my inbox. I've subscribed and look forward to reading future posts!

This one in particular sparked my interest to dive deeper